The Nickel Market: Investing Ahead of the Crowd – Part 2

In Part 1 of this report, we discussed the nickel supply fundamentals and identified important factors that can help to indicate where nickel supply is headed. To refresh your memory, here are a couple of the most important factors:

- The partial Indonesian ban on nickel exports should continue as the country looks to develop its smelting industry.

- The Philippines have suspended or closed roughly 50% of its annual nickel production due to environmental concerns. In 2016, the Philippines were the world’s largest nickel producer, given the current direction of government policy, and the fact that their nickel output is down 24% year-over-year in 2017, this will not be the case in 2017.

- Analysts from Scotia and RBC Capital Markets expect nickel supply to grow at 2% per annum until 2020.

- Total global nickel inventories are trending downwards, falling 15% to below 500,000 tonnes, since hitting a high in April of 2016.

Source: RBC Capital Markets

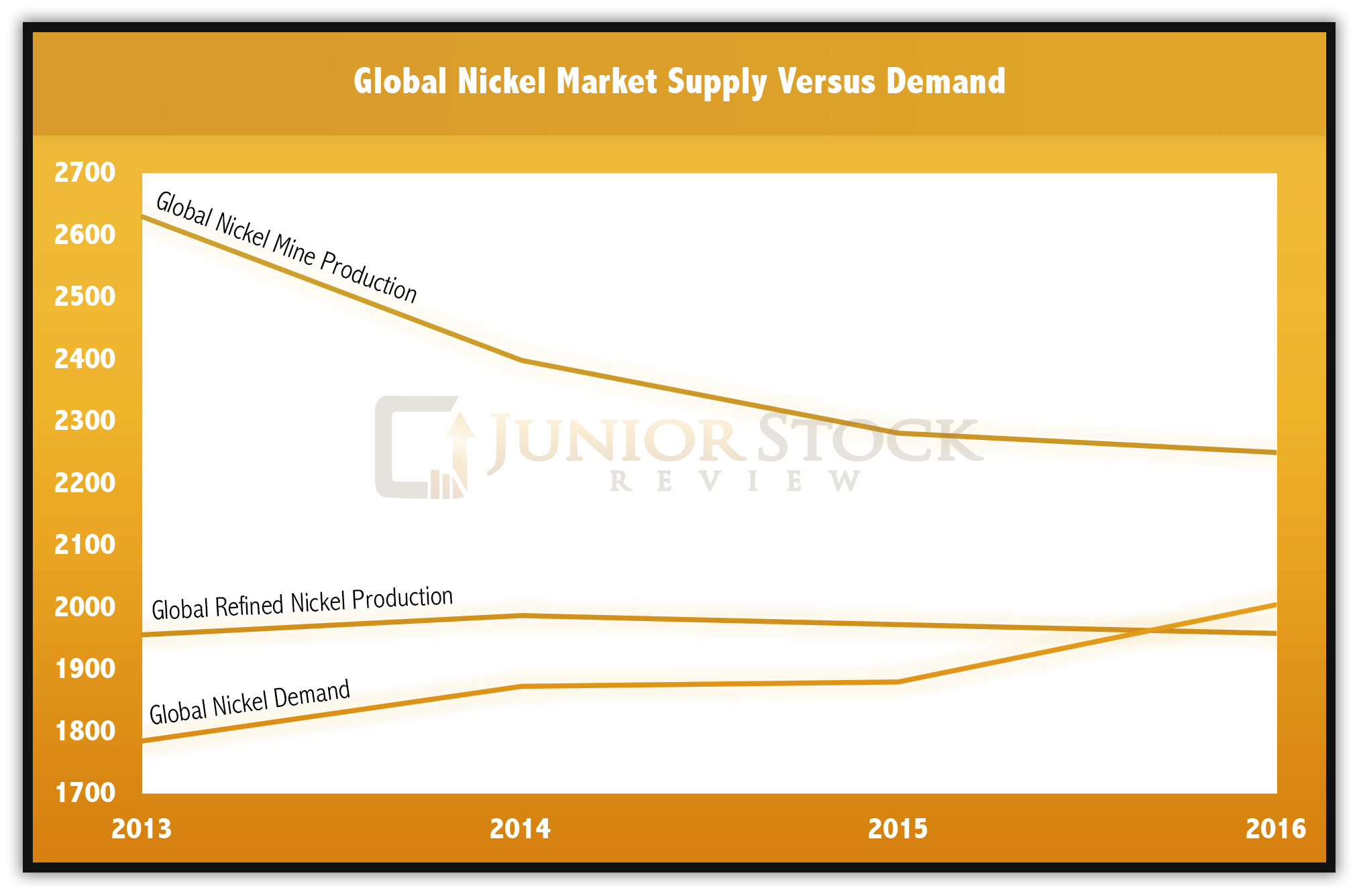

Let’s take a look at nickel demand, by first examining the refined production, which includes LME-grade nickel and host of intermediate nickel products such as NPI, nickel concentrate, ferronickel, nickel sulphate and more.

The Refined Nickel Supply

Source: RBC Capital Markets

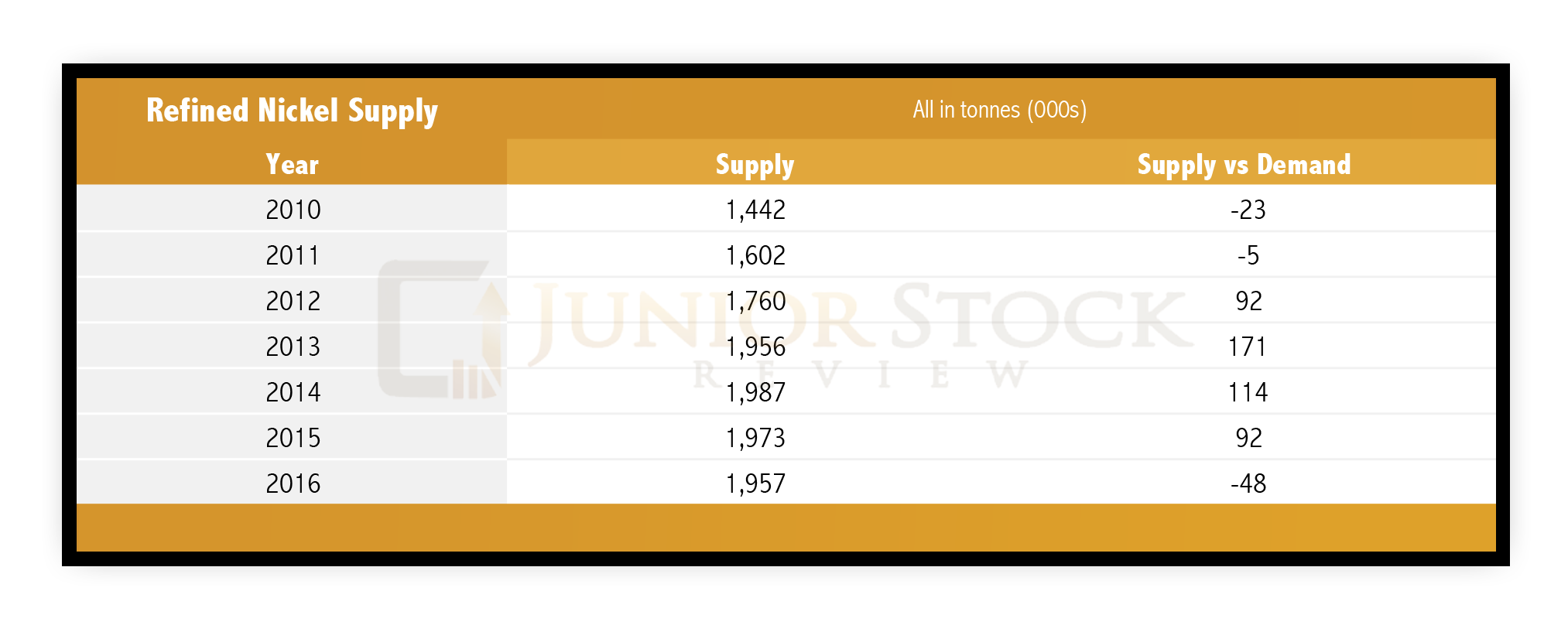

The global refined nickel supply for 2016 was around 1.9 million tonnes, which was 48,000 tonnes below the global demand. Of the 1.9 million tonnes of refined nickel, 44% is produced by former Eastern Bloc countries. Given their less stringent environmental laws and overall lower cost structure, the former Eastern Bloc countries dominate the nickel ore refinement industry.

The global refined nickel capacity is estimated to be around 3.2 million tons. Putting it into perspective, current mine production is sitting at around 2.25 million tons, which is roughly 30% of the global refined capacity. However, note that the bulk of the capacity is in China and their figures, in my opinion, should not be taken as 100% valid.

The future of the global refined nickel industry will be shaped by a few key developments over the coming years.

Indonesian Ban and its Effect on Refinement

As discussed in Part 1, the global landscape for refinement changed in 2014 when the Indonesian government banned the export of its nickel ore in favour of promoting investment in refinement facilities within its borders.

Indonesia’s nickel refinement capacity has spiked dramatically since 2013, moving from around 10,000 tons in 2013 to over 100,000 tons in 2016. This new capacity mainly replaces capacity in China, as China’s refined nickel production has fallen by around 7% since the export ban.

The Environment vs. Metal Refinement

Currently, China has suspended the use of heavily polluting smelting operations in both the nickel and zinc industry. This is proof that air quality is becoming a leading political issue, even in states which typically buck the current political trends of the rest of the world. Time will tell how this will play out in the nickel market, especially in the face of what looks to be growing demand.

Interestingly, much of the nickel demand in the future is projected to come from electric vehicles (EV). The irony of the EV movement, in terms of it being non-carbon emitting, is the fact that the vast majority of the materials which make up the EV are all mined and refined, which is exactly what some countries are trying to curtail. I suppose you can’t have your cake and eat it, too.

Nickel Production Cost Curves

A cost curve is a graphical analysis which plots production capacity versus the costs of the entire industry. The cost curve is an important piece in the analysis of commodities as it allows the curious investor to see how the current spot price of the chosen metal fits in with the current cost of production across the sector.

Companies that find their cost of production in the lowest quartiles of the cost curve are those least likely to be affected by low spot prices. The nickel market has been plagued with low spot prices for a number of years, due to excess supply, but as we saw last year, this is changing.

RBC Capital Market’s cost curve for the nickel industry reveals that the 75th percentile of the industry’s cash cost is $5.05 USD/lbs, meaning that 25% of the world’s nickel producers will have negative cash flows as a result of $5.05 USD/lbs spot price.

Generally, for a healthy market, analysts look to the 90th percentile of the cost curve to suggest an sustainable price. In terms of the nickel market, the 90th percentile represents a cost of production of $7.85 USD/lbs.

Compared to today’s nickel spot price of around $5.17 USD/lbs, that is a 50% increase to reach a level in which 90% of producers will be able to produce nickel at a profit.

A Conversation with Martin Turenne

As in Part 1, I had the chance to ask FPX Nickel Corp. CEO, Martin Turenne, a series of questions pertaining to the global nickel market. Highlights from our interview will be shared throughout the report.

![]()

FPX Nickel Corp. (FPX:TSXV)

MCAP – $16.1 million CAD (at the time of writing)

CEO – Martin Turenne

Question #1

Brian: In every industry, the success of a company or sector is based around the delta between the cost of production and the selling price, or more simply, the amount of profit. Given that the current nickel price is roughly $5.17 USD/lbs, roughly 25% of the nickel industry’s producers are not making money.

In your opinion, what are the 3 biggest factors affecting the nickel spot price, and will their resolution lead the nickel spot price up to what many analysts believe is the key long-term price for nickel producers, roughly $7.85 USD/lbs?

Martin: The overall theme driving the price higher is the fact that nickel demand is exceeding supply, and will continue to do so well into the 2020s. The first reason for that is strong demand growth. In 2016, nickel demand was 6% higher than the previous year, which was by far the highest demand growth among the major base metals. I expect to see continued demand growth in that range for the next several years.

The second reason has to do with nickel supply growth, which is going to be relatively weak. Because nickel has been so badly beat up, and because there has been so little investment in nickel exploration and development, there just aren’t many new projects which can be brought into production in the next five to eight years. I’d argue this is a more acute issue for nickel than it is for metals like zinc and copper, which have attracted far more capital in recent years.

Finally, I think you will see operating costs increase in the coming years. In the past several years, operating costs in the mining industry have been declining mostly due to a strong U.S. dollar and lower energy costs. Going forward, a decrease in the U.S. dollar or increase in oil prices will lift the nickel cost curve, and thus lift the nickel price.

Nickel Demand

So far, we’ve covered the global nickel mine supply/production figures and also taken a look at global nickel refining numbers and the factors affecting their markets. The last piece of the puzzle is nickel demand, the how and why it’s used in society and where I believe it’s headed.

It isn’t a stretch to say that nickel is one of the most important industrial metals in the world. It’s used in construction, power generation/storage, food preparation, cell phones and vehicles. Nickel has a unique blend of properties such as corrosion resistance, high strength, and toughness.

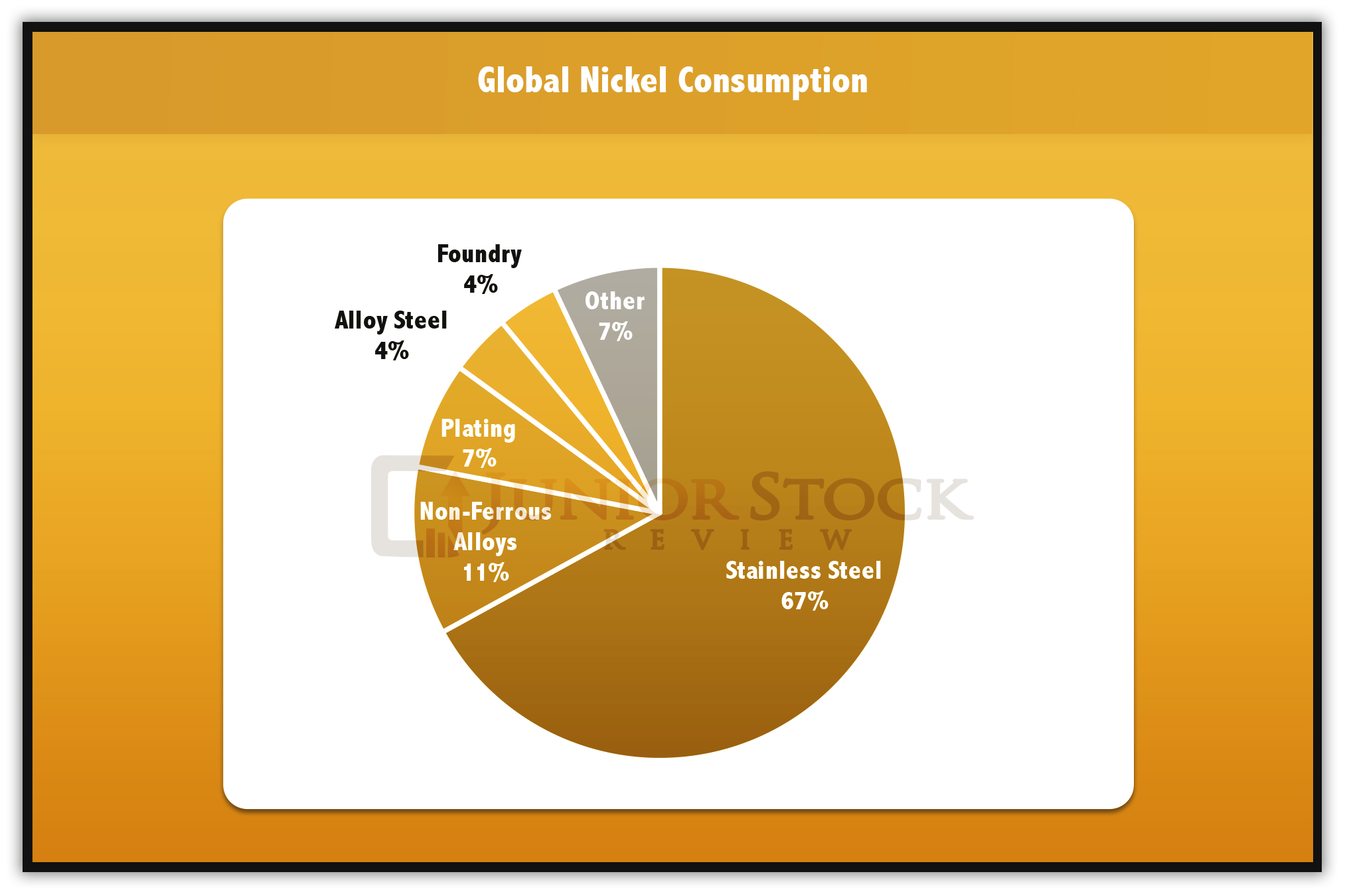

World Nickel Consumption

Source: RBC Capital Markets

Question #2

Brian: 2/3 of refined nickel is consumed by stainless steel, the remainder is broken down into much smaller demand sources. This demand pattern has existed for refined nickel consumption for a while now.

How do you view the future of refined nickel demand? Will stainless steel still be the dominant consumer or are there other sources of consumption which may begin to play a bigger role? Please explain.

Martin: Among all the major base metals, nickel had the best growth profile in 2016, with demand rising 6% compared to 2015 demand. Going forward, analysts are predicting annual demand growth in the 2-3% range, which in my view is too conservative. Stainless demand will continue to play a dominant role in nickel, but the growth associated with electric vehicle (“EV”) batteries will be the big story over the next decade. Right now, EV battery nickel demand is approximately 70,000 tonnes per year, or only about 3% of total nickel demand. Going forward, Roskill predicts that number could reach 400,000 tonnes per year by 2025, which implies an average demand growth rate of 2% per year for nickel from EV battery demand alone. From today’s levels, I can see nickel demand growing 5% per year for the next several years, which would likely push the nickel price well above the current consensus number.

Stainless Steel

As you can see, 2/3 of refined nickel is used in the production of stainless steel, while a further 15% is used in the manufacturing of other ferrous and non-ferrous alloys. Stainless steel is an alloy of traditional steel and the combination of nickel and chromium, typically with 8 to 12 percent nickel content.

Stainless steel’s uses are numerous, ranging from cookware to appliances, building materials and high-tech applications. The stainless or corrosion resistant properties are homogenous or consistent across the entire section of steel, giving it a huge advantage against the other corrosion resistant materials which are mainly coatings.

From a food preparation or eating perspective, there currently isn’t any other material that can withstand the temperature ranges, pHs, bacteria exposure or repeated usage like stainless steel. Utensils, cookware, appliances and food prep surfaces all use stainless steel as the preferred material of choice.

The Use of Stainless Steel in Marine Infrastructure Construction

Stainless steel may get a huge boost in the near future as a few of the southern States (US) look to increase the grade of rebar used within all of their marine construction. For those who don’t know, my background is in steel manufacturing. I was General Foreman of operations at a rolling mill which produced rebar, angles, channels and flats.

Typically, concrete / rebar construction is designed with a 25 to 50 year life span, however, marine construction, in particular, has come under scrutiny for not being robust enough, which has prompted some States to look at increasing the construction specifications for the materials used in marine construction. For rebar, this means higher grade requirements and possibly being restricted to only corrosion resistant steel.

Currently, epoxy coated rebar is used for applications that require corrosion resistance, however, epoxy coatings have been known to crack, allowing for moisture to begin its oxidation of the steel.

Also, galvanized steel is an option for this application, as it, too, provides a corrosion resistant coating to the rebar. However, like the epoxy coating, it’s susceptible to wear and damage and a worn or damaged zinc layer leaves the under body of the steel product vulnerable to moisture.

Without a doubt, construction is moving toward more stringent regulations for the structures being built in our cities. I believe one of the big winners of this movement will be the strong corrosion resistant materials, which are headlined by stainless steel.

Electric Vehicles

Arguably the largest catalyst for a major increase in nickel demand is the rise of electric vehicles or, more specifically, the use of batteries in our vehicles. As we discussed in the factors affecting the mining and smelting of nickel, the environment is a major political issue, one that is currently centred around clean air.

Governments around the world are pushing us toward a goal of reducing the amount of carbon we emit into the atmosphere. One of the first industries to feel this disruptive wave is the automotive sector, which has seen government subsidies for electric vehicles (EV) propel companies such as Tesla into the forefront of both the automotive industry and popular culture.

The culmination of these events has sent all of the other major automotive companies spinning as they try and catch up to a growing segment of the market.

Batteries

While nickel is used in a variety of ways in vehicles, by far its biggest use is within an EV, where it’s used in the batteries. Currently, the misnomer is that a lithium ion battery is primarily made up of lithium, but the fact is, it isn’t. Lithium ion batteries contain more nickel, cobalt and manganese than they do lithium.

Nickel’s current use within the EV market is very small, especially when compared to global nickel demand. However, it’s the potential that we must gauge when it comes to nickel demand in batteries, not the EV market’s current consumption.

Lithium Ion Batteries

Depending on the application, currently, what makes up the cathodes for the most common lithium Ion battery is nickel, manganese and cobalt (NMC), or nickel, cobalt and aluminium (NCA) and an anode typically composed of graphite. To note, the cathode does contain other materials such as lithium, but in smaller quantities than the big 3.

For those unfamiliar with how batteries work, here’s a quick summary; there are three basic components to most batteries: cathode, anode and electrolyte. A chemical reaction causes a charge difference between the anode and cathode. This charge difference allows the electrons (electrical current) to flow between the anode and cathode and, in the process, the electrical current powers the piece of equipment to which the battery is attached.

A number of sources, including the Battery University, confirm that the NMC battery is the battery of choice when it comes to power tools and other electrical power trains. The cathode chemical composition is chosen on 4 key criteria: stability of materials, energy density, specific energy and cost.

Today, NMC batteries are typically found with compositions of equal parts, denoted 1-1-1, but have started to be made in ratios as high as 8-1-1. Due to higher cobalt prices and security of supply, the percentage of nickel is beginning to move higher.

Interestingly, depending on the applications, cobalt can be reduced and still maintain acceptable performance, as the higher percentage nickel batteries have higher energy densities and longer life spans, although, they produce a lower voltage.

Lastly, it should be noted that roughly only 50% of the current nickel mine supply is suitable for battery use, as the low-grade nickel products are inadequate for battery manufacturing. Given that nickel mine supply growth is mainly in NPI and FeNi, which are low grade products, it would appear that available supply for the emerging battery market is fixed at its current production rate. Considering this fact, it is apparent that a growing battery sector will certainly have an effect on the nickel market.

Projected Nickel Demand Via EV Batteries

Worldwide, Statista says that since 2014, on average, there have been 73.7 million cars sold each year. According to Inside EVs, in 2016, 777,497 EVs were sold worldwide. Considering that just 5 years previous only 17,425 EVs were sold, this gives us a Compound Annual Growth Rate (CAGR) of 88.33%.

Therefore, using the EV CAGR and projecting out until 2021, you get a demand of 18.4 million electric vehicles.

Now that we have determined the possible future demand for EVs, it is possible to calculate the amount of nickel which these EVS will require. To do this, I will use a figure published by Glencore on their twitter account, which states that,

“Every new #electricvehicle – from its motor & batteries, to the charging point will need c.160kg of copper, 11kg of cobalt & 11kg of nickel.” ~ Twitter – Sept. 7, 2017

Clearly Glencore is using a NMC battery configuration of 1-1-1, which I believe should give us a conservative estimate of future nickel demand.

Therefore, if 18.4 million EVs are sold in 2021, the amount of nickel demand is calculated by:

18.4 million EVs x 11 kg Ni/EV = 202,400,000 kg of Ni

202.4 million kg of Ni x 1/1016.05 kg = 199,203.4 tonnes of Ni

199,203.4 tonnes of Ni / 1,957,000 tonnes of Ni (2016 mine production) = 10% of 2016 mine production

This is just a rough calculation with a couple assumptions, however, it does give us perspective on how powerful and disruptive this clean air policy trend can be. If the nickel market was hit with 199K tonnes of high grade nickel demand in the next few years, it would put tremendous pressure on the market, and in my opinion would result in higher nickel prices.

Dramatic price spikes in the nickel spot price will cause battery manufacturers to look for alternatives to nickel. This won’t happen overnight, but it’s pertinent to expect battery improvements along the way that may reduce or eliminate the amount of nickel used within the battery composition, just as manufacturers are reducing the cobalt portion of the batteries to compensate for higher cobalt prices.

Concluding Remarks

Question #3

Brian: Putting it altogether, there are a few key aspects of the nickel market which need to be watched in order to gauge where the nickel market is headed in the near term. That said, still contend that the future is bright for nickel.

Can you give us one final concluding comment on the nickel market, how you believe the narrative plays out and, ultimately, where the nickel market is headed in the next 12 months?

Martin: The spot price has made a huge move since mid-June, going up 35%, but since the base metals marked their bottom in January 2016, nickel is still lagging the price moves made by copper and zinc. Going forward, I expect to see nickel continue to play catch-up with those metals, largely because demand continues to exceed supply by a large margin. If we assume continued, steady mine production from Indonesia and the Philippines, the nickel market will continue to be in deficit and the spot price should be supported. But, if we see any further actions to restrict production in those countries, there’s potential for another explosive move upward. In either case, FPX Nickel is very well-positioned to capitalize on an increasing spot price with the ongoing advancement of our Decar project in British Columbia, which we believe is the finest development-stage nickel asset in the world.

It’s my contention that nickel will continue to play a major role in our everyday lives, as its uses continue to grow. Let me summarize my thoughts in a few key points:

- Watch the actions of the Philippine government closely, as their choice to ban nickel ore exports and/or suspend/close mining operations within its borders will have major implications on the nickel ore supply.

- Government environmental policy, particularly that associated with air pollution, will affect the nickel market in two ways: First, it will constrain supply as both the Philippines and China suspend/close operations. Second , it will create demand for nickel via the emerging EV automotive sector.

- Infrastructure building regulations will only get more stringent as government looks to extend the life spans of their structures past 50 years. Corrosion resistant steels will play major roles in this trend, with stainless steel leading the pack.

- Current nickel spot prices leave 25% of the nickel producers in negative cash flow. If this trend continues, producers will go out of business and supply will fall further. A rise in the nickel price isn’t necessarily imminent, but it’s inevitable.

- Global nickel inventories are falling, but are still high relative to current production. Watch for continued drops in inventory levels, as it is my guess that the Philippine government will move forward with their decision to ban nickel ore exports.

- High-grade nickel demand is set to grow in the future, as the EV market continues to grow worldwide.

While there are a few key aspects to watch, I still contend that the future is bright for nickel and will be looking for opportunities to invest ahead of the crowd.

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company(s) and sector that is best suited for your personal investment criteria. Junior Stock Review does not guarantee the accuracy of any of the analytics used in this report. I do own FPX Nickel Corp. shares. I have NOT been compensated to write this article.