Currently, a bullish thesis on oil is met with concerns about an impending recession.

It’s understandable, the market isn’t great right now.

The fear of the unknown can be troubling.

Especially when it comes to investing.

If you think that you can buy something cheaper in the future, it’s only natural to want to wait.

However, the problem is twofold.

First, will what you are predicting even happen?

When market perception is almost unanimous, in my experience, it usually doesn’t play out exactly the way you think it will.

Second, let’s say it does, the recession or crisis hits.

Will you have the courage to buy when things continue to erode or drop quickly?

Maybe, but again, in my experience, that mindset tends to lead the investor into thinking that a share price might go even lower – I’ll wait!

Buying when others are fearful is necessary as an investor, but it’s not easy.

Looking back on my own experience, I was able to muster the courage to buy tranches in good companies amidst the chaos of the falling market in 2020.

It’s this dollar cost averaging approach which gave me the best of both worlds.

Yes, this approach reduced my upside, but most importantly, it reduced my downside.

Courage doesn’t mean you are without fear…

It means that despite the fear, you logically move forward and execute.

Not surprisingly, 2020 was my most profitable year, thus far.

Buy in the bearish depths, have patience, and in years like 2016 and 2020, there is potential to make a lot of money.

Speaking of the 2020 Covid-19 pandemic, it’s easily the most cited example to refute buying oil and oil-related equities at today’s prices.

2020 was a traumatic year for many, not only oil investors.

But the situation in 2023 is not the same as 2020.

In 2020, the world was shut down due to Covid-19.

People across the world were locked down in their homes.

They weren’t driving to work, taking their kids to school, going to the movies or taking a holiday in the Caribbean.

Life as we knew it changed to the extreme during those early days of the Covid-19 pandemic.

Certainly in my lifetime, and arguably in the history of the world, humanity had never experienced something of this magnitude.

In response to this extraordinary event, the oil price for a short period of time went negative.

In essence, suppliers had to pay to get rid of their barrels of oil.

It’s a crazy thought.

Something I still have a hard time wrapping my head around.

In my view, the recency of that event hasn’t been forgotten by investors.

Today, I think it’s that risk of recession that has everyone in a state of fear.

Asking themselves, ‘how low can or will it go?’

It’s an appropriate question, but if your recency bias is toward the negative, obviously you are going to say, ‘very low.’

Maybe even jumping to the extreme conclusion that this is it, the end.

I can’t predict the future, but I will say that I think it’s unlikely that this is the end and I doubt that we will see a negative oil price anytime soon.

In my view, the Covid-19 pandemic was a unique event, one that may indeed happen again, but we won’t get to plan for it.

It’ll just happen…

If we are heading into a recession, yes I think it has the capacity to be a doozie, but we’re still going to consume oil.

Most of the people who live in the developed world are highly dependent on oil or natural gas in their daily lives.

Electricity generation, fuel for their cars, and a whole host of petroleum products – plastics, etc. are all consumed each and every day.

Consumption amounts may diminish, but they won’t disappear.

This is even more true for the developing world, whose sole reliance is almost exclusively linked to oil and its derivatives.

I do think in a recessionary setting the oil price can go lower, but I don’t think it will stay there for long.

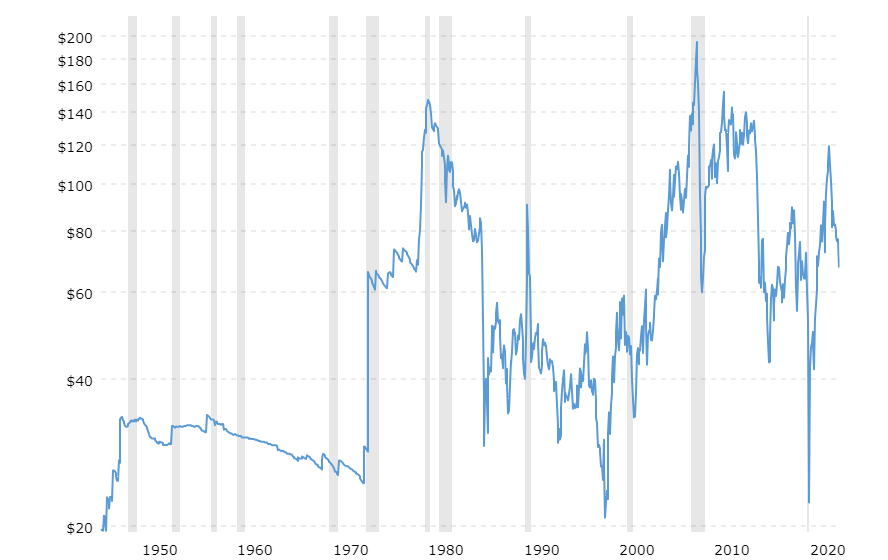

Examining the oil price chart above, you can see the volatility we have seen over the last 70 years.

The recessions are highlighted in gray.

There is no real pattern that I can see that depicts how the oil price behaves during and after recessions as none of them are the same.

The oil market is extremely complex.

In my view, looking back at past performance doesn’t give us any indication of how things will work today.

The situations are totally different.

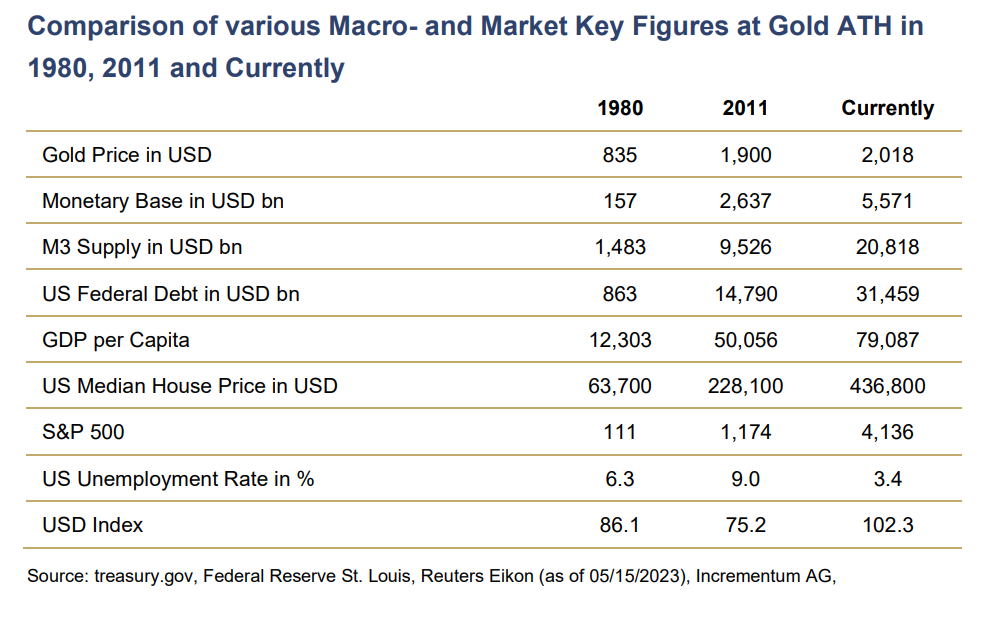

Look at this table from IGWT’s 2023 report regarding a few metrics in relation to the 1980s, 2010s and today;

As you can see, these various decades are completely different, incomparable, unless you are trying to point out how different they are.

Add in demographics, geopolitics, interest rates and a number of other factors and today we live at a distinct moment in time.

We have to evaluate today with today’s known metrics.

Let’s start with interest rates.

In my view, the Central Banks, mainly the U.S. Federal Reserve (FED), will deploy the same tactics that we have seen in past crises or recession moments.

Quantitative Easing (QE) is their desired remedy to a downturn.

I don’t think that changes anytime soon.

In 2020, the Covid-19 pandemic was met with unprecedented spending.

More money was infused into the system in 2020 than had ever been created in all previous years COMBINED!

A recession appears to be coming, how bad it will be is still a question mark.

Either way, I still think we’re in the mindset of expanding the money supply to combat the pain of economic turmoil.

Therefore, when you mix in the lack of oil exploration and development, war in Europe (escalating?), OPEC+ production cuts and the depletion of the U.S. Strategic Oil Reserves, I think the oil price recovers quickly – V Shaped.

We live in a world that is still very much dependent on oil and all of its derivatives.

We are fortunately or unfortunately multi-trillions of dollars and a whole bunch of years away from meaningfully cutting our dependency.

To me, US$70/bbl is much closer to a bottom in the oil price than a top.

Ergo the opportunity.

Opportunity in the resource market is usually accompanied by patience.

We’ll see where the oil price goes.

In the meantime, you should become a Junior Stock Review VIP and get my latest thoughts on the resource sector sent right to your inbox for free.

For no particular reason, I have always concentrated my resource sector speculations on the hard rock juniors.

Hard rock mineral exploration and development has an allure that most other sectors can’t compete with.

In particular, the anticipation for drilling and discovery success can incite copious amounts of greed from the market.

In this regard, it’s arguably the gold companies that garner the most attention.

It’s the portion of the sector that first grabbed and kept my attention all these years.

That said, all exploration comes with major risks to your investment dollars.

Risk factors range from those associated with jurisdiction – permitting, taxes & social unrest, to exploration failure, to poor market sentiment and/or technical failure – metallurgical, geo-technical, etc.

There is always the risk to lose it all.

Another often overlooked risk to your cash is the “dead money” risk.

Dead money represents an investment in a junior whose share price is stuck in a tight range for a prolonged period of time.

There can be a number of reasons why this happens.

For example, it could be a drawn out permitting process.

The market loses interest and then often sells or, possibly worse, forgets about it.

Dead money mixed with low liquidity means you’re stuck.

Your investment dollars aren’t able to move into new opportunities and, given the rising cost of inflation, you’re actually silently losing your purchasing power with those dollars.

Dead money is tough because it’s a risk across the sector.

On a whole, the juniors are mostly illiquid and even the best companies can have stretches where their share price doesn’t move.

That isn’t always a problem, but when you mix it with bad news, it can be terrible.

As an investor, I think you can develop a framework of decision making to minimize this, but never eliminate it.

Which brings me to the topic I wanted to discuss today, the merits for investment in oil and gas companies.

Oil exploration and development companies are susceptible to the same risks as hard rock companies, with one slight difference.

A junior oil exploration company moves from explorer to producer on the same day of discovery, while for a hard rock company, the discovery just marks the beginning of what is usually a long path to production.

Hard rock discoveries must go through resource delineation, further financing, environmental studies and permitting.

This process can often take 10+ years.

Those years in between are the ones where those risks I spoke about earlier can come back to bite you.

Now, don’t get me wrong, I love speculating in hard rock exploration and development, these comments are not meant to dissuade you.

I continue to be a hard rock junior company investor.

I’m merely pointing out a difference and what is a big reason why I’m so attracted to the oil and gas space, right now.

As an added bonus, I’m very bullish on oil.

Late last year, my interest in the sector was sparked by a friend’s investment in a tiny western Canadian oil junior.

After a site visit, some good conversation and a whole ton of research, I’m convinced that the oil price is headed to uncomfortably high levels in the future.

When exactly you might ask?

I wish I knew, but I don’t.

While I can’t tell you when, I can take you through some of the factors that I think will propel the oil price higher in the future.

From there, you can decide for yourself.

To me, the story starts with the pace of financial and social change worldwide.

In my view, it’s quickening.

Major transitions in society, especially those related to commodity consumption, mark huge opportunities to make money, on both the old and new side of the trade.

The biggest shift in commodity consumption is the transition away from fossil fuels, mainly oil, to renewables or non-carbon emitting sources of energy.

This is a monumental challenge, one that will undoubtedly be rocky and take much longer to execute than many may think.

Moreover, while the Western nations try to virtue signal their way politically away from fossil fuels, they can’t escape the fact that their bottom lines are still highly tied to the oil market.

Today, the ESG investment movement has pushed investors, banks and funds away from the oil companies.

Further, it has forced oil companies to further cut exploration and development of new wells and, instead, shift a portion of their development dollars into renewable energy sources.

While this trend, at first glance, would seem detrimental to the oil price, it’s in fact just the opposite.

In my view, it will lead to supply constraints and, ultimately, much higher sustained oil prices in the future.

If you’re bullish on the world’s electrification, you have to be bullish on oil.

Fortunately or unfortunately, the two go hand in hand.

In my view, this is an opportunity for investors who can see through the politics and realize that our dependence on oil is far from being over.

ESG investment policies and electrification diminish the supply side of the oil market.

Further, there are a bunch of other factors that I believe will drive the oil higher, such as:

Rise of the 3rd World (Developing nations)

OPEC production cuts

Lack of new oil exploration & development

High interest rates

Depletion of the US Strategic Oil Reserves

War – Russian Sanctions, Petro Yuang and BRICS+

I can’t cover all of these bullish factors in one article.

It’s going to take a few to discuss all of these points in detail.

So stay tuned.

In the meantime, you should become a Junior Stock Review VIP and get my latest thoughts on the resource sector sent right to your inbox for free.

What is the first thing that pops into your mind when you think about Argentina?

For some, it’s Lionel Messi or football (soccer for those in North America).

For others, it’s beef; I’ve been told that Argentina’s steakhouses are among the best in the world.

For investors, it’s most likely a thought about risk.

So why do investors associate Argentina with risk?

Since the 1930s, there have been issues with Argentina’s economy.

It has been a constant struggle to manage its national debt, control inflation, and now, within the last 20 years, deal with the consequences of a default on the national debt in 2001.

Going back to the early 90s, Argentina dealt with their inflation issue by pegging the peso, at par, with the U.S. dollar.

Further, the government privatized numerous state-owned and operated businesses to stimulate the economy and, of course, provide a much needed boost to the government’s treasury.

In 1998, however, things began to unwind, as debt continued to grow and the boom created by the privatization of the state-owned companies diminished.

Over the next 3 years, things progressively got worse, and eventually, it led to Argentina’s now famous default on their national debt in 2001 – roughly US$93 billion.

The situation spiralled out of control.

The peso took a massive hit.

Bank deposits were frozen.

The unemployment rate rose to over 22% and social unrest followed.

From this point onward, the country has never really been able to “right the ship†as they say.

To be honest, it really doesn’t surprise me, either.

As debt levels begin to rise and reach or exceed that of GDP, historically speaking, there is no turning back.

Not only is rising debt an issue from an economic standpoint, but socially, easy money becomes a part of the culture – it’s hard to break.

Applying this to Argentina’s situation, I really see no discernible changes in the obviously flawed government policy that led to this mess.

You can’t fix a debt issue with the same policies that created the issue in the first place.

Like so many countries, these days, governments have let their debt load rise to a point where they can’t even service the interest (at reasonable rates) on the debt.

Rather than default, governments or central banks choose to lower interest rates and begin the process of spurring inflation.

Inflation, however, like most things in life, is a double-edged sword.

Yes, you are able to inflate away your debt by de-valuing your currency, but it comes at a high cost.

First, you can’t control it.

Inflation isn’t like a light, you can’t turn it on and off at will.

Second, inflating away debt destroys the middle class, the very people whom government’s say they are trying to help.

SIDE NOTE: It’s estimated that Argentina’s annual inflation is an astounding 40%. Remember, the U.S. Federal Reserve has openly stated on numerous occasions now that it wants to trigger inflation within the U.S. economy. Inflation will devalue the USD and, over time, allow payback and the servicing of the national debt. I understand the intrigue of the idea, but the fact is, it can’t be controlled and, unfortunately, comes at a huge cost. Readers take note of the situation in Argentina and the numerous other examples we have seen throughout history. None of the situations are exactly alike, some worse than others. Bottom line, it doesn’t ever end well for the average Joe.

It’s a crazy, never ending loop.

While Argentina is particularly bad at managing its debt, it isn’t alone.

Most of the world, especially due to the Covid-19 pandemic, has elevated their debt levels to realms that are impossible to service at healthy or normal interest rates.

We are truly living at an interesting juncture in human history.

So, with this in mind, as resource investors I think that there are 2 main questions that need to be asked.

The Current Situation

First, from an economic standpoint, what is the current situation in Argentina?

Argentina continues to struggle with its current financial situation.

They have defaulted on their debt for a ninth time since 2001 and have an economy which is estimated to contract by 12% in 2020.

The latest default is linked to a US$57B IMF bailout in 2018, which, at the time, was coined as a ‘standby financing’ which would allow the economy to recover and put Argentina in a position to begin paying off their debt.

The economic recovery didn’t happen and the Covid-19 pandemic certainly hasn’t helped, but is hardly the main reason for the failure.

It’s obvious that this is a continuous loop of defaults, inflation and bailouts.

SIDE NOTE: Argentina’s international credit rating with Standard & Poor, Fitch and Moody’s is ranked alongside countries like Ecuador, Venezuela, Lebanon, and Congo. These aren’t the countries you want to be associated with when it comes to economic prosperity.

In eerily similar fashion, today, Argentina is in the midst of negotiations with the IMF on restructuring their debt and delaying payback until 2024.

This is a key negotiation for both parties.

From the IMF’s view, they just want to get paid, and there’s nothing wrong with that.

My guess is that the IMF wants to find terms that don’t completely tie the Argentine government’s hands, but are stiff enough to prevent the chance of another default in the future.

As the Argentine government states, they don’t want to default on their debt and this is why they are looking for further wiggle room in the payback structure.

In my view, prevention of a future default on debt is inextricably linked to a cut in government spending – without a doubt.

With that said, given their past and the fact that there are midterm elections on the horizon, I find it highly unlikely that this will happen.

The government, however, has announced new stiffer capital controls, in addition to those adopted in 2019, which are aimed at stabilizing the country’s foreign currency reserves.

The foreign currency reserves, mainly their holdings of USD, are vitally important because their debt is denominated by USD.

Citizens are being dissuaded from purchasing USD and selling pesos, and at the moment, they can only acquire a maximum of US$200 per month.

Further, there’s a new 35% tax on USD denominated purchases, which is on top of the 30% solidarity tax that’s already in place.

Corporations, like Argentina’s citizens, are subject to similar controls that are aimed at diminishing the export of USD.

This mainly affects how companies distribute dividends, export goods and service their USD denominated debt, although new recent regulations were recently put in place to solve these issues, as mentioned below.

SIDE NOTE: The Peso is losing its value at such a high rate that nothing of significant value is priced in it – Real estate, vehicles or any other big ticket items are all priced in USD.

With rampant inflation and stringent capital controls, a black market for USD has sprung up.

The official exchange rate – 74ish Pesos to 1 USD.

The unofficial or black market rate – 150ish Pesos to 1 USD – and rising fast.

As you can see, for those looking to acquire more dollars or dollar denominated services/products, the cost is enormous.

Moreover, these restrictions, while bringing short-term stability to the foreign currency reserves, without a doubt, have cast further doubts about the investment attractiveness of Argentina.

Mining Investment Attractiveness of Argentina

So now, as resource sector investors, what’s the current mining investment attractiveness of Argentina?

This is a great question and the whole point of this article.

The fact is, if you just read the headlines surrounding the current risk in Argentina, you would be missing a big part of the equation.

As always, there’s never a ubiquitous answer to any question, it always depends.

In this case, it depends on:

Type of Company – At the moment, junior mining companies that are exploring and/or developing projects are able to take advantage of the unofficial exchange rate between the Peso and U.S. dollar by completing what some of the companies call a “Blue Chip Swap (BCS)â€.

A BCS is when a company imports USD into the country and invests it into blue chip stocks on the Argentine exchange.

After holding it for a period of time, they then liquidate the position and are able to take the cash out and convert it at the unofficial exchange rate – completely legal.

To note, all the companies that I spoke with use the official rate to set budgets.

For companies that only burn cash, this is a major plus.

For producing companies, it’s a little different.

As I stated earlier, there are restrictions on USD out flows – dividends, profits and debt payments.

With that said, the government has relaxed some of the restrictions in light of the importance of mining.

Reduce the export duty for mining exports from 12% on FOB value to 8%

Include mining activity in the strategic plan for the reactivation of the Argentine Economy.

Further, the Central Bank Of Argentina (BCRA) stated the following in ‘Communicacion A 7123’:

Foreign currency brought into Argentina and liquidated into pesos by export companies will enable those companies to: (i) pay off capital and interest of foreign loans (provided that repayment terms are greater than one year) and (ii) repatriate capital, which we understand includes dividends, from investment projects once they have started operations.

All this is subject to certain conditions (that the mining industry meets) such as the following: 1. The exports refer to productive projects that generate export goods and / or that allow substituting the import of goods; 2. The foreign currency from exports is entered into the country as from October 2, 2020; 3. Those who opt for this regime designate a financial entity that will do the follow-up. For those who opt for this regime, the amounts of foreign currency that they will be able to acquire for imports are also increased (50% of what is exported).

Location – As they say in real estate “location, location, location,†and the statement applies to the junior mining world.

As I mentioned in Part 1 of the series, it’s key to understand the risks at the national level and work your way progressively down to the state or province then to the region or county, and finally, at the local town or city level.

As you progress toward the exact location of a prospective company’s project, you will uncover any hidden risks at the upper levels.

In terms of Argentina, it’s all about which province the project is located.

San Juan and Salta, in particular, are great provinces in which to be a mining company.

Both have the history, mining law and general positive attitude toward mining.

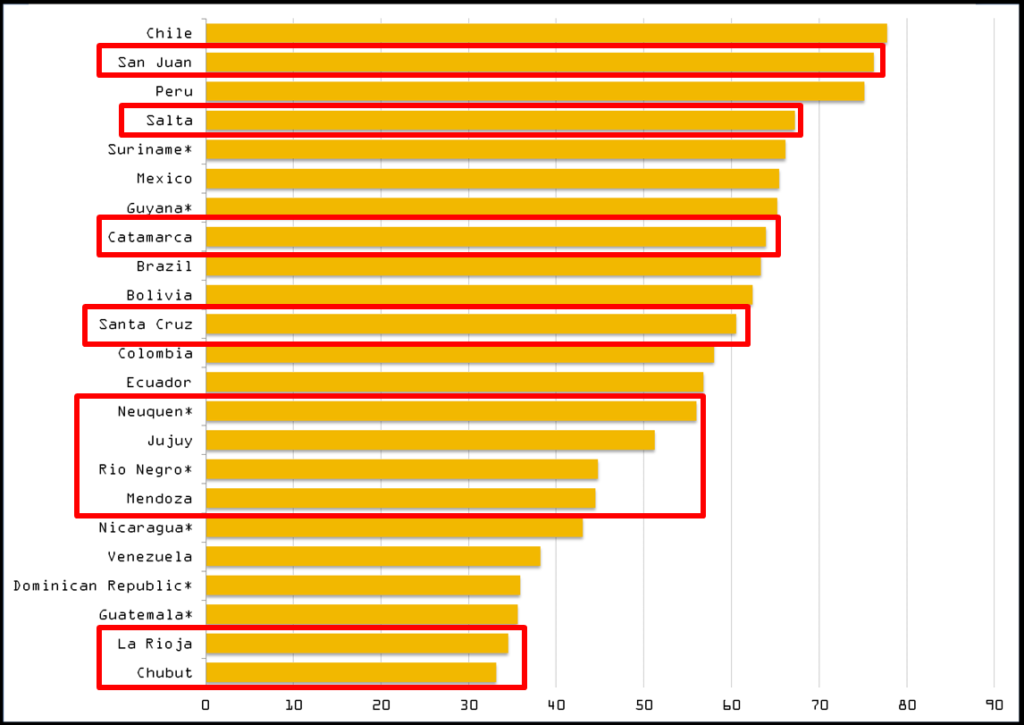

Here’s a look at how the Fraser Institute ranks mining investment attractiveness in Latin America.

Source: 2020 Fraser Institute Rankings

As you can see, San Juan and Salta are ranked #2 and #4 in Latin America and only trail Chile and Peru, which are widely considered some of the best places in the world for mining investment.

In Argentina, the provinces control the mining law and collection of taxes, which are capped at 3% of revenue.

Now that we have an idea of Argentina’s current situation and how it affects junior mining companies, it’s pertinent to explore risks that may occur in the future.

I think there are 3 main risk factors that we need to explore:

Nationalization of Assets – The nationalization of assets is a very real risk.

Unfortunately for investors in the resource sector, it does happen and, more specifically with Argentina, it has happened once fairly recently.

In 2012, the Argentine government voted to re-nationalize the country’s largest oil company, YPF.

For context, YPF was once an entirely state-owned company until the spree of privatization in the 90s, which resulted in a large portion of the company being sold off to foreign interests.

At the time, Christina Fernandez de Kirchner (now VP under Alberto Fernandez) was President and justified the re-nationalization on the grounds that the private company didn’t boost the oil and natural gas production needed to keep up with local demand.

This move has and will continue to haunt Argentina moving forward.

So, are junior mining companies at risk of having their projects or mines nationalized?

No one can say ‘yes’ or ‘no’ without a doubt.

What I will say is that at least a portion of the risk is dependent upon the type of company.

In my view, the companies that are exploring or developing a project(s) in Argentina are less likely to see their projects nationalized than a producing mine.

Junior mining companies require both cash to burn and a niche skill set to effectively explore and develop projects.

I highly doubt this is an appealing prospect to a government.

Second, while the risk is higher for producing hard rock miners, I still think that there are many barriers to making nationalization an appealing alternative for governments.

Why nationalize and have to operate a mine when you can just tax it?

Further, while YPF is a recent example of nationalization in Argentina, I wasn’t able to find an example of a fully private company that was nationalized by the government.

While I know the government is fully capable of stealing, I’m less inclined to believe that is the course of action they would prefer to take.

New Tax Regime – It’s my contention that the greatest risk to mining companies within Argentina is the risk of increased taxes in the future.

A new tax regime could remove a good portion, if not all, of the profitability of a mine.

How likely is it to happen?

That’s a really hard question to answer.

There are a couple of scenarios that I think could make taking a larger chunk of the mining company profits tempting.

A major spike in the metal prices – In my view, mining is one of the few sectors that I think will show major growth over the next few years. This growth will be driven by high metal prices.

Brink of another default – As I mentioned, I don’t see any dramatic policy changes related to spending coming anytime soon. This is a problem moving forward as it appears that their current loop of borrow, inflate, and default will most likely continue into the future without a drastic change to how the country is run.

While the threat of higher taxes is a risk to mining companies in Argentina, it may only be a threat to future mines.

It should be noted that junior mining companies, by current law, lock in tax rates for 30 years of production once a Feasibility Study (FS) has been completed on their project.

Now, this doesn’t mean laws can’t be changed – they can be.

But I can’t help but think that the fallout of such measures would cause much more damage than any short-term gain.

Ecuador is a great example for Argentina.

Their institution of a windfall tax had devastating effects on the mining sector.

With a new government in place, the impact of the windfall tax was re-assessed and, with the help of Wood Mackenzie, Ecuador revamped their tax regime to better reflect best practices worldwide.

Low and behold, investment dollars from investors and major mining companies have begun to flow back into the country.

Ecuador is by no means a perfect jurisdiction for mining, but it’s getting better and has outstanding geological potential.

Mining is a huge part of Argentina’s economy, especially in provinces like San Juan and Salta where mining accounts for more than 80% of the province’s revenue.

They can hardly afford to lose it.

For perspective, for every US$1 that leaves the country because of mining, US$24 comes in.

Higher taxes on mining aren’t the answer to Argentina’s debt issues.

If anything, the government should make it a priority to enhance Argentina’s mining investment attractiveness, not further destroy it.

In the end, I think that the provinces that are pro-mining and have a history of upholding its mining law will remain that way.

With regards to the Federal government, it’s much harder to gauge.

Mining Companies in Argentina

Many of the biggest senior gold and silver miners have operations or are developing mines in Argentina.

Here’s a list of a few of them:

Pan American Silver (PAAS:TSX) – Operate their Manantial Espejo mine in Santa Cruz and owns the Navidad project in Chubut.

Fortuna Silver (FVI:TSX) – Recently spent US$300M in CAPEX to construct their Lindero Mine, which is located in Salta.

Barrick Gold (ABX:TSX) – Operate their Veladero mine and the Lama project and new exploration areas in San Juan. In 2020, Barrick also entered the Salta province by signing an earn-in agreement on the El Quevar silver project.

SSR Mining (SSR:TSX) – Operate Puna which is comprised of the Chinchillas mine and Pirquitas processing facility which is located in Jujuy.

Newmont (NGT:TSX) – Operates the Cerro Negro mine in Santa Cruz.

McEwen Mining (MUX:TSX) – Operate their San Jose silver-gold mine in Santa Cruz jointly with the Peruvian company Hochschild, and also owns the large-scale Los Azules copper project in San Juan.

Yamana (YRI:TSX) – Operate their Cerro Moro in Santa Cruz.

Austral Gold (AGD:ASX) – Operate their Casposo mine in San Juan.

First Quantum Mineral Ltd. (FM:TSX) – Advancing their Taca Taca project in Salta.

Glencore PLC (GLEN:LSE) – Operate Bajo de la Alumbrera project in Catamarca, jointly with Goldcorp and Yamana Gold, and also owns Pachon in San Juan.

A few junior mining companies that are exploring and developing projects in Argentina:

AbraPlata Resources (ABRA:TSXV) – PEA Level Project

Filo Mining Corp. (FIL:TSXV) – PFS Level Project

Aldebaran Resources (ALDE:TSXV)

Golden Arrow Resources (GRG:TSXV)

Neo Lithium (NLC:TSXV)

Lithium Americas Corp. (LAC:TSE) – Under construction

Concluding Remarks

In my view, protecting your downside risk by investing in companies that are selling for less than their value is an essential part of making money consistently in the junior resource sector.

The higher the delta between price and value, the more downside protection you have.

I believe, therefore, that it allows for investment in opportunities in some of the riskiest jurisdictions on the planet.

Now, there’s a thin line here, you do have to understand what you are getting into and how the company you are investing in is going to navigate that risk and, ultimately, make you money.

There are going to be some situations that just aren’t worth the risk or the time commitment.

Personally, I think that I have a good understanding of the situation in Argentina.

There is risk.

With that said, I’m ready to make investments in junior mining companies operating there if they fit my framework for an investable company.

As always, the thesis starts with the people running the company.

Do they have the IQ, experience and backing to execute the action plan which they are pitching?

Second, if it’s the right people, is the company selling at a discount to its value?

The higher the discount to value, the more appealing the opportunity is.

Third, where is the project located?

Personally, I want to concentrate on San Juan and Salta.

I put my money where my mouth is and have put this framework to use.

Last year, I invested in AbraPlata Resources at $0.033/share.

It’s run by the right people.

At the time of investment, the company was selling for a steep discount to value.

Finally, their Diablillos project is located in Salta.

All the right ingredients needed to protect my downside risk, plus it had huge upside potential if the company executes on their plan.

Today, the share price is roughly $0.38, a more than 10 fold increase and, at the moment, a vindication of the original investment thesis.

Investing your money in countries like Argentina come with risk, but if you have done your homework and have applied a framework for decision making, it’s my contention that you have given yourself the best opportunity to be successful.

Finally, there’s nothing wrong with avoiding risky jurisdictions, just remember any country/government is capable of stealing your money.

Use the Coupon Code DILIGENT to get 25% off a subscription to and get my best investment ideas and commentary first.

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review Premium

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria

Our success in life is largely due to the quality of the decisions we make.

The more consistently we make good decisions, the better chance we have of achieving our personal goals.

So why do some people tend to make good decisions consistently?

This is a great question.

I think the answer is that some people have better frameworks for making decisions than others.

For some, these frameworks come naturally, it’s just the way that they think.

For others, it often requires a conscious decision to follow a framework for their decision making, which, of course, is influenced by what they want to achieve.

The more scattered or unfocused your goals, the weaker your framework is for decision making and the more susceptible you will be to emotional states of mind.

Be very specific with what you want in your life and, more pertinent to this article, what you want out of your investments.

This will dictate the ideal framework for your investment decisions.

It’s clear to me that the core reason I have lost money in the market, in the past, is directly related to the poor decisions that I’ve made.

Unfortunately, mistakes will happen, no one is perfect.

With this said, my personal goal is to both reduce the number and severity of the losses in the future.

Thus, as I’ve stated, I created and use a set of rules to anchor my thoughts and decisions regarding my investments.

My framework and adherence to that framework for decision making in the junior resource sector is better than the average investor.

I’m, therefore, able to minimize my mistakes and, consequently, am able to profit consistently no matter what market we’re in.

Today, I would like to discuss a particularly important subject when it comes to junior resource sector investment – jurisdictional risk.

Unlike many other types of businesses, mineral deposits or mines can’t be moved if a country suddenly becomes a place where it’s hard or impossible to do business.

The assessment of risk within a jurisdiction, therefore, is an integral part of a junior resource sector investor’s decision framework.

While it’s integral, in my view, it isn’t where you should start.

Personally, I think you begin your investigation with answering the following question; what is the delta between price and value?

Buying a company which is trading for less than its value is the overriding principle that must be followed continually to ensure success in the junior resource sector.

Once you have determined that a company is selling for less than it’s worth, you proceed to contrast that value proposition against the risk to investment.

Putting it together, if you personally think that the value proposition contrasted against the downside risk is acceptable, you should be a buyer.

It’s easier said than done.

Identifying and understanding the risks are a big part of being successful.

As I said, employing a system or framework for analysis can drastically improve your rate of success and, ultimately, minimize your biggest risk to your investment – YOURSELF!

Let’s take a closer look at some of the points to consider when constructing your framework for analyzing jurisdictional risk.

A Framework for Analyzing Jurisdictional Risk

Jurisdictional risk is a complex topic.

With that said, I think breaking it up into individual components is a great way to simplify the analysis.

For me, I think there are 3 main components:

Mineral Potential

Geography and infrastructure

Political Risk

Law

Culture

Influences – dominant religion(s), genesis of the country, demographics, etc.

Geography

Timing

Flow of Cash – Smart money is typically paying close attention to the timing aspect.

Mineral Potential

Why do junior resource companies explore for mineral deposits in some of the world’s riskiest jurisdictions?

The answer is straightforward; for the most part, all of the large, outcropping, easy-to-find deposits in tier #1 jurisdictions have already been found.

It’s, therefore, the probability of making a big discovery which drives exploration teams to take their drills to these far flung locales.

Further, mineral potential can be gauged by looking at historical discoveries in the region or by simply looking at a map and looking for areas with high geological activity, such as mountain chains.

The potential or the actual size and quality of the deposit should be at the forefront of every resource sector investor’s mind.

Taking it a little further, while the mineral potential is first and foremost, infrastructure can be a major hurdle to overcome, even for the best deposits.

Road access, power, water, and deep sea ports are all major factors contributing to not only the discovery of new deposits, but also the conversion of those deposits into mines.

Both the mineral potential and infrastructure quality are inputs for computing a project’s underlying value, which can then be contrasted against the company’s market price.

The delta between these values will allow you to understand the value proposition.

Political Risk

There aren’t many topics that get more complex or emotional than those focused on political risk.

Political risk breaks down further into a number of sub-topics:

Law – The rule of law within a jurisdiction is very important as it should clearly outline the criteria for ownership, taxation and liability. It’s important to research a jurisdiction’s past and current reputation for upholding the laws that it’s supposed to be governed by.

Culture – This is where things get complex, as a country’s culture is formed over hundreds of years by numerous inputs. Inputs such as the dominant religions, demographics, how and when the country was formed, and much more. What you see is what you get. Don’t expect a cultural shift in your lifetime. Things may appear to be changing or shifting in a direction, but much like markets, there’s always a reversion to the mean.

Geography – The location and terrain of a nation play a big role in its risk profile. For instance, if a country is land locked, this could be an issue for travel, the importing of exploration equipment, or future export of mineral concentrates. Further, if the country is located next to a high risk country which is dominated by a terrorist organization, civil war or a virus outbreak – these issues can plague neighbouring nations.

Timing

Much like markets, in my view, jurisdictional risk moves in a cyclical motion.

The risk is always there, but it can change briefly after extremes in risk are realized.

Such as after a civil war, the fall of a dictator or on the less extreme end of things, the mass exodus of mining companies due to a new and damaging tax regime.

As I have said many times, it’s impossible to time markets with any consistency.

Sticking with the comparison of markets to the cyclicality of jurisdictional risk, I think that it’s very hard to try and pick a bottom.

What I suggest is that investors don’t try and pick the bottom, let someone else do that.

Look for smart or big money entering a risky jurisdiction after one of those climax-like events happen.

Smart or big money can be named investors putting a large chunk of cash into a junior, or maybe it’s a senior mining company which is buying a project they’re looking to develop on the cheap.

It’s a really good sign for investors in junior companies when a senior mining company sinks big dollars into a project to turn it into a mine.

Fraser Institute

While certainly not being perfect or the definitive source, the Fraser Institute does a great job at quantifying jurisdictional risk in their annual rankings of Mining Investment Attractiveness.

I continually reference the rankings as part of my research into a jurisdiction.

They are free to access and review; I highly suggest adding this to your investor tool kit.

Concluding Remarks

Jurisdictional risk is a huge topic, one that actually requires much more depth than I covered in this article.

Further, I think to really understand the topic, you need to do more than just a desktop review, you really need to visit the country in question.

It isn’t until you visit a country that you can begin to understand the culture and the nuances that come with it.

Further, while much of the jurisdictional risk discussion revolves around countries, you must really drill down to the local level of the project.

Start at the country level and move down to state or province, then move down to county or region, and finally, move down to the immediate locale – town or city.

It’s here where you can find a whole other sub-culture, one which most likely has its own nuances.

With the knowledge gained from this article, you can begin to form your own framework for analyzing jurisdictional risk.

Creating the framework and doing the research puts you miles ahead of the average investor in the junior resource sector.

It’s that advantage which will give you a leg up when it comes to becoming consistently successful with your investment choices.

In Part 2 of the series, I will use the framework laid out in this article to analyze a specific country.

Stay tuned.

Get the e-book Junior Resource Sector Investing Success: The Risks, Rules & Strategies You Need to Know today, when you become a FREE Junior Stock Review VIP .

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review Premium

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria

In the junior resource sector, people are everything.

Find the right people and, more often than not, you will have found a successful investment.

For me, I met FPX Nickel Corp.’s CEO Martin Turenne in the summer of 2018 and, right then and there, I knew I’d met someone worth investing in.

Turenne is as good as CEOs get in the junior mining sector – Intelligence, Integrity and Drive.

To date, FPX has generated an 800% return for myself and my subscribers, and I believe it has the potential to reach much higher levels in the future.

In our conversation, Turenne gives his opinion on the current nickel market, an overview of the recently released updated PEA on FPX’s Baptiste project and, finally, outlines FPX’s plan for the next 6 to 12 months.

Enjoy!

Brian: The Covid-19 pandemic has affected the mining industry, shutting down or drastically reducing production from a number of different mining operations worldwide.

In terms of supply, has the Covid-19 pandemic affected the worldwide nickel supply, and if so, how?

Martin: Earlier in the year, there was significant disruption to nickel mine supply in the Philippines and temporary shutdowns of certain nickel operations in Canada and Madagascar – at one point, approximately 20% of nickel mine supply was off-line. Even with the restart of most of those operations, BMO recently noted that, taking into account disruptions to both nickel supply and demand owing to the pandemic, it expects nickel demand to exceed nickel mine supply this year. However, BMO also expects that refined nickel supply (including refining of previously stockpiled nickel ore) will exceed demand in 2020.

Brian: Measuring the impact of the Covid-19 pandemic on the metal’s supply fundamentals is fairly straightforward. When it comes to demand, however, the answer is a little more ambiguous.

I will split this next question into 2 parts.

First, in your view, regarding present or near-term nickel demand, has the Covid-19 pandemic affected nickel demand, and if so, how?

Martin: The pandemic has resulted in an approximate 5-10% reduction in most nickel analysts’ 2020 demand projections versus what they had been forecasting before the pandemic – so this removes approximately 100-200 kt of demand from 2020. As the year goes on, and as Chinese demand continues to surprise to the upside, we expect that demand disruption to be closer to 5% than 10%.

Brian: Second, it seems to me that the long-term effect of the pandemic on nickel demand could be much different than the near term.

With many questions still surrounding near-term nickel demand, how do you view the long-term nickel demand thesis; are EVs at the core of a bullish future?

Martin: Yes and no. Stainless steel demand accounts for approximately two-thirds (or approximately 1.5 million tonnes per year) of total nickel demand, so this will continue to drive overall demand growth in the short-term. According to Shanghai Metal Market, stainless steel output is only down 1.7% year-to-date – this is more robust than most analysts predicted in light of the pandemic. Remember that stainless growth has averaged 5% CAGR over the last 5- and 15-year periods and has always surprised to the upside versus analyst expectations. If stainless grows by 5% per year, this adds about 75 kt per year of new demand to the market.

In terms of EVs, they represent about 5% of nickel demand, or approximately 100 kt per year. BMO figures this number will reach about 160 kt by 2023, or an incremental 20 kt or so per year. There will be a massive impact from EV demand on nickel, but it likely won’t reach that “hockey stick” growth phase until 2025 or so.

Brian: The nickel market has attracted a lot of attention over the last few months and, in my opinion, it is directly related to a few comments by Billionaire Tesla Founder, Elon Musk.

Musk made a reference to nickel during one of Tesla’s post-earnings conference calls saying,

“Tesla will give you a giant contract for a long period of time, if you mine nickel efficiently and in an environmentally sensitive way.”

In your opinion, have Musk’s comments had an effect on the nickel market? If so, please explain.

Martin: Yes, they have. Among his many other qualities, Musk might be the best market promoter of all-time, so his call for “green” nickel has raised a huge amount of investor interest in nickel. In order to keep the cost of EV batteries (and therefore of EVs themselves) low, Tesla and other carmakers need a lot of nickel at the lowest possible price – because the price of nickel is a key driver of battery pack cost. His comments also highlight the fact that nickel is, in general, a highly carbon-emitting and polluting industry, so his call for “green” nickel really places a spotlight on the need for responsible practices in this sector – and that’s where we think Canadian projects like ours have a big advantage over nickel production in places like Russia, Indonesia and the Philippine.

For the first time in more than a decade, we are starting to see mainstream, generalist interest in nickel. For investors looking for nickel exposure, the landscape of nickel equities is very small, and generally constrained to smallcap companies like ours with market caps under $200 million. There’s potentially a lot of capital out there waiting to be deployed into a relatively small number of investable nickel companies.

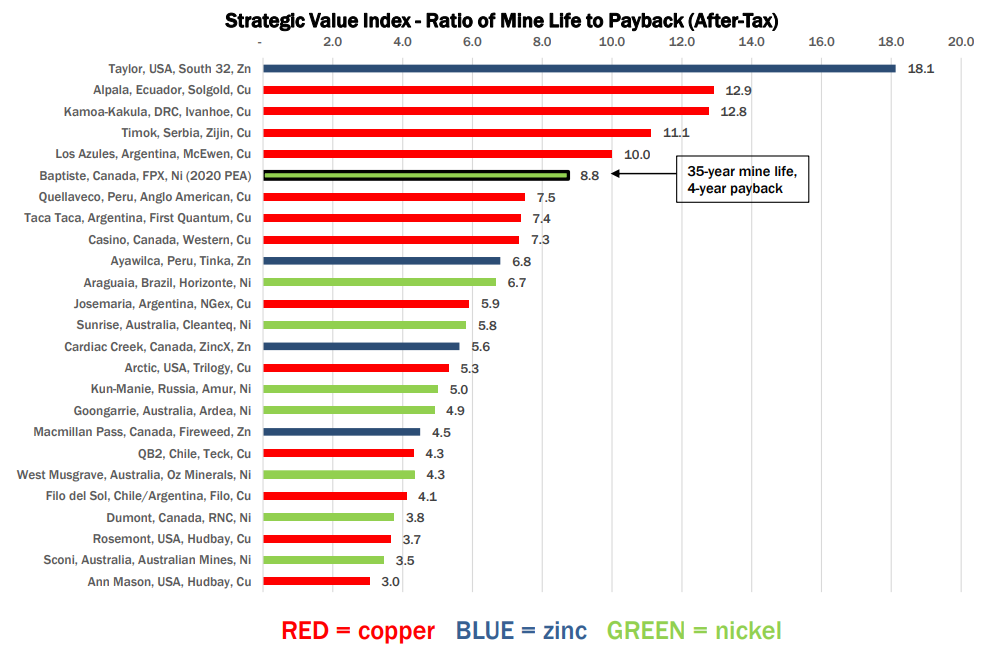

Brian: The updated PEA results on FPX’s Baptiste project were just announced and I think they look great. In fact, better than I had guessed.

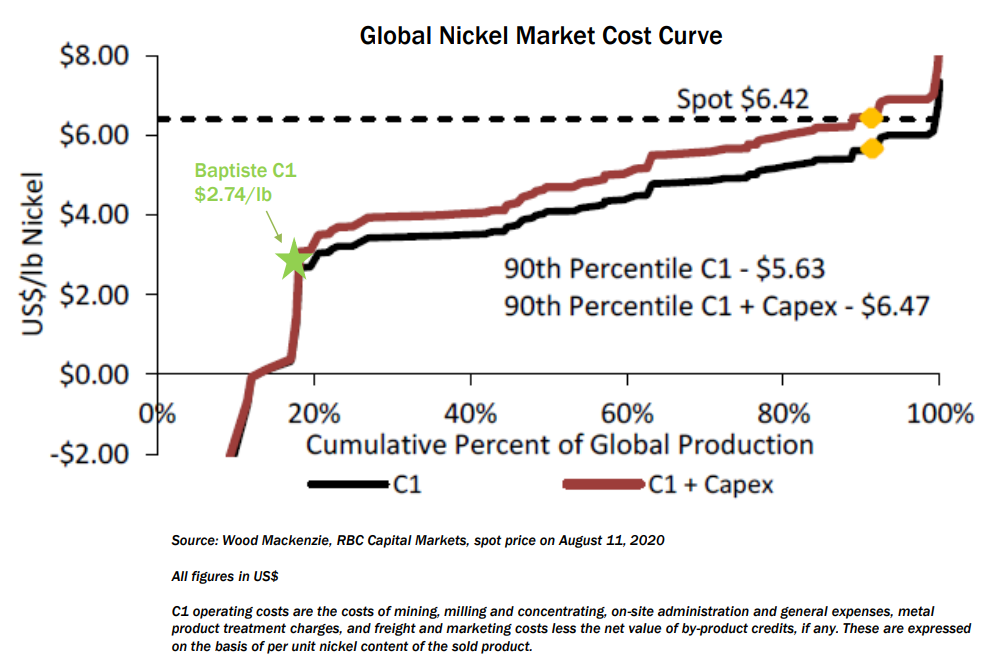

A few of the highlights – An after-tax NPV of US$1.7 billion, 35 year mine life, 1st quartile operating costs of US$2.74/lbs Ni and AISC of US$3.21/lbs Ni.

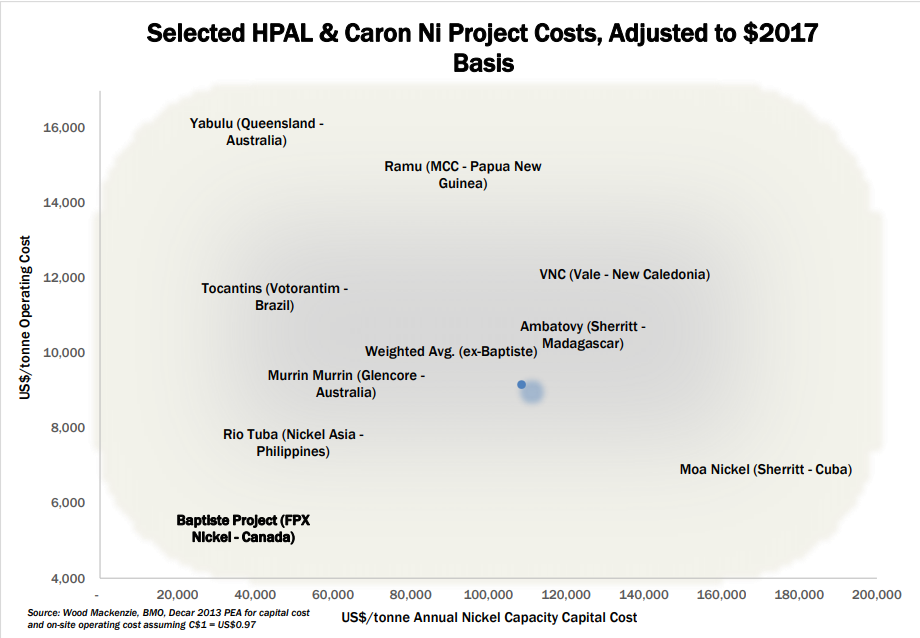

On the other side of the coin, some investors may be concerned with the upfront CAPEX cost of US$1.6 billion and, coincidently, the low after-tax IRR of 18.5%.

Martin, first, can you review the highlights as you see them from the updated PEA?

Martin: The PEA really highlights the huge strategic value of Baptiste. First, with annual output of 99 million pounds per annum, this could be one of the 10 largest nickel mines in the world. Second, the very long mine life (35 years) provides exposure to multiple up cycles in the nickel market, which as you know can be a volatile market with big swings between price highs and lows. With C1 operating costs at US$2.74/lb, Baptiste would sit in the bottom quartile of the industry cost curve, and thus provide margin protection even in periods of very low commodity prices. Finally, the fact that our testwork has demonstrated the potential to produce nickel for both the stainless market and the EV market – this really emphasizes the strategic long-term flexibility of the project for decades to come.

Brian: Following that, can you please address the concerns over the upfront CAPEX and IRR? I believe it needs further context.

Martin: On CAPEX, building large nickel projects is very much like building large porphyry copper projects – these are inherently capital-intensive industries. During the last cycle of nickel mine construction from 2010 to 2013, major companies like BHP, Glencore and Vale built nickel mines at an average capital cost of US$4 billion. So while the CAPEX for Baptiste is by no means low, it is, actually relatively modest in the comparison to the CAPEX for other large nickel operations – either those build during the last cycle, or those projected for the next cycle.

In terms of IRR, it helps to understand the typical “hurdle rates” that major companies use to guide their mine construction decisions on large projects. An IRR over 10-12%, this is considered a strong rate of return for a large, multi-generational asset – so at over 18%, Baptiste is actually very robust given the scale of the project and duration of the project. Remember that IRR and NPV are discounting metrics – they apply a discount rate to future cash flows, so any free cash flow beyond the first 10 years of operations are heavily discounted and add very little to IRR and NPV calculations.

Brian: It isn’t a stretch to believe that the world is headed toward more stringent environmental controls. Musk’s comments are a great example of how culture shapes the direction of corporate culture.

In terms of FPX, UBC and Trent University are currently completing a study on the Baptiste deposit waste rock, which they believe may have the capacity to sequester carbon.

Can you give us an update on the study and explain how carbon sequestering, if possible, could play a large role in a future mining operation?

Martin: A few nickel companies are starting to talk about the potential for developing zero-carbon operations, but we are really taking the lead in terms of testwork and publishing data to support these claims. Our Baptiste deposit is uniquely rich in a mineral called brucite; when brucite is exposed to air in the context of a tailings facility, the mineral will naturally absorb carbon dioxide from air and sequester the CO2 in mineral form forever. The researchers at UBC and Trent University believe that Baptiste has high potential to sequester enough CO2 to completely offset the carbon footprint of the mining operation, making this a carbon neutral operation. We will be publishing test data in the coming months to support the potential for this to become a reality.

When you consider Baptiste’s scale and strong economics, and then factor in its potential to be a low- or zero-carbon project, we believe this could be very important in attracting interest from investors working under an ESG mandate, and also major mining companies, most of whom have committed to making their operations carbon neutral in the coming decades.

Brian: With the updated PEA now behind you, what is the priority for FPX over the next 6 to 12 months?

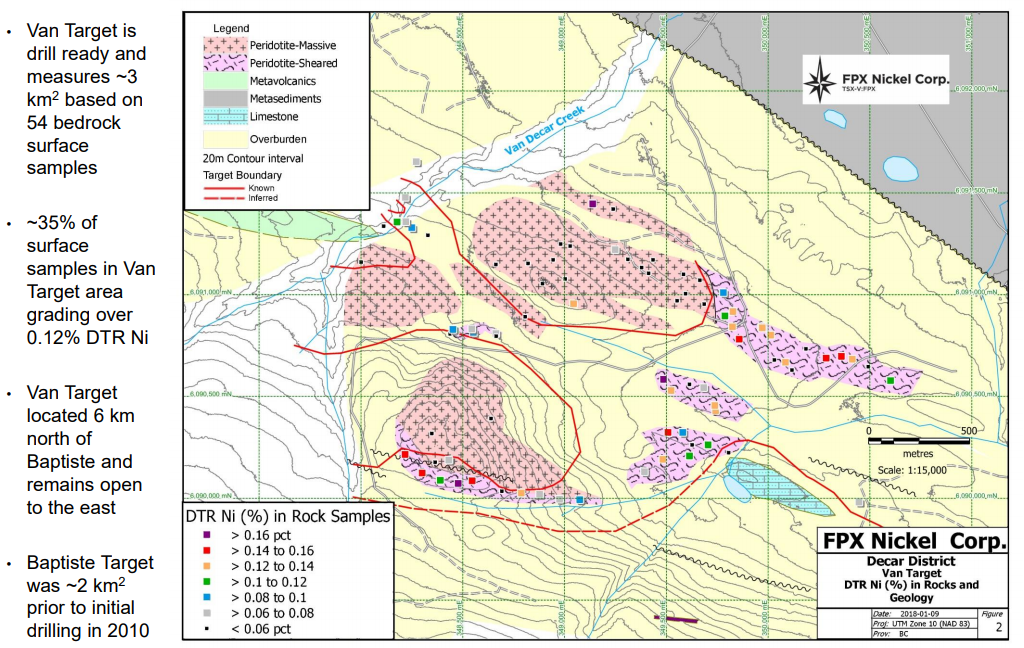

Martin: We have a dual-track strategy. First, we will advance Baptiste into the initial stages of a preliminary feasibility study, with a big focus on metallurgical test work and market testing of nickel products for both the stainless steel and EV battery markets. Second, we would like to undertake a drilling program at the Van target, which sits 6 km north of Baptiste within our 245-square km land package at Decar. Baptiste has a lateral footprint of 2.5 square km of mineralization; at Van, we have already delineated a 3 square km footprint of outcropping bedrock mineralization, with stronger grades at surface than those at Baptiste. The Van target has never been drilled, but we think there’s a strong possibility that it could prove larger and/or higher grade than Baptiste, and that we could delineate a second world-scale nickel orebody to truly make Decar a multi-generational nickel district with the scale and mine life potential that approaches the Sudbury complex. The PEA has already demonstrated that Baptiste is one of the most robust large-scale nickel deposits in the world – we’re really excited to see if Van can be even better than Baptiste in that regard.

Prior to the 2019 edition of the Sprott Natural Resource

Symposium, I

mentioned that Rick Rule’s speech on Thursday August 1st would

be worth the price of admission – he didn’t disappoint!

The speech was entitled, Lessons,

Re-Learned, In a Bear Market, and for good reason, as Rule covered many of

the lessons that I have found so helpful over the course of my investing

career.

Here’s a look at 2 lessons that, when incorporated into your

investment process, in my view, will be key to your success.

The

sequence of answering unanswered questions leads to high returns over time.

This lesson is the basis for share price

appreciation across all sectors, but is particularly important in the junior

resource sector.

So, given its importance, how does one

identify a company’s unanswered questions?

The unanswered questions focus on the

catalysts that will drive the share price in the future, for example, the most

common unanswered questions surround drill results.

Invariably, the answering of these questions

leads to more unanswered questions and, thus, the process really never ends

until you get a “no” answer or you have attained an acceptable amount of profit

(different for everyone).

Along with identifying the unanswered

questions, it’s paramount that the investor evaluate the probability of attaining

a “yes” answer to each of the questions and weigh it against the potential

profit.

Evaluating the probability of success is

rooted in the company’s fundamentals, aspects such as who is running the

company, its share structure, its cash position, the geology of the property

and the jurisdiction in which the company is operating – to name just a

few.

Examples of unanswered questions:

Question – Does the mineralization extend

along strike from the existing deposit?

If yes, how far and at what grade?

Question – Is the mineralization amenable

to standard mineral processing techniques – crushing, grinding, floatation,

magnetic separation?

If yes, are there any deleterious elements

contained in the concentrate?

If yes, what are smelter penalties?

If yes, what is the metal recovery?

Share prices are driven by catalysts, and

by focusing on these quantifiable answers, an investor can not only maximize

his potential profit, but also minimize the effect that emotion has on their

investments.

When the reason to own a

stock goes away, the stock needs to go away.

Lesson #2 is closely linked with

lesson #1, but is particularly important in my opinion because selling a losing

position can be hard to do.

The basis of this lesson is

rooted in selling a stock because of receiving a “no” answer to an unanswered

question. In my experience, this is very wise advice, especially in the short

term, as it most often takes time for a company to reset and recover after

failure.

Additionally, I think you can

parlay lesson #2 a little further.

For example, you may invest in a

company for specific reasons, such as its business model, the involvement of a

particular person, its focus on a particular metal, or maybe it’s an interest

in a particular project.

Following the mantra of lesson

#2, if any of these reasons change, it’s time to sell. For example, if a

project generation company whose business model centres around using “other

people’s money” to explore their properties changes to using their own money to

explore, you may want to think about selling, as the risk profile of the

company just changed.

In my view, these lessons are invaluable and, when

practiced, easily justify the price of admission to a conference such as the

Sprott Natural Resource Symposium.

With that said, it will be 2020 before you know it, and with

it a chance to register for next year’s conference at a significant discount if

done early. Watch for the links in the New Year.

Symposium Exhibitors

One of the many perks of attending the Symposium is its list

of exhibitors, each of which has been vetted by the Sprott organization and

owned in a Sprott managed equity account.

While this is definitely an advantage, it doesn’t mean that

investors should freely invest in any company at the conference. No matter who

recommends a company, each investor is obligated, in my view, to complete their

own due diligence and determine if it’s an investment which fits their own

personal criteria.

I met with 10 companies that were exhibiting at the

Symposium and compiled a few notes on each of them. In no particular order:

Aethon Minerals (AET:TSXV)

MCAP – $5 million (at the time of writing)

Cash – Over $3 million

Altius Minerals (ALS:TSX) spin out in 2018.

Recently announced a merger with AbraPlata,

whereby all of the issued and outstanding Aethon shares will be exchanged on

the basis of 3.75 AbraPlata common shares for each Aethon share. This implies

consideration of $0.248 per Aethon Based on the 10-day volume weighted average

of AbraPlata shares $0.661.

Currently, Aethon is trading at discount to

AbraPlata.

John Miniotis will be the new company’s

President and CEO.

Flagship asset – the Diabillos Project has a

total indicated resource of 27,100 tonnes – 80.9 million oz of silver at 93.1

g/t and 732k oz of gold at 0.84 g/t and an inferred resource of 1,100 tonnes –

1.69 million oz of silver at 48.8 g/t and 29K of gold at 0.83 g/t.

Diabillos Project – High grade precious metal

exploration potential.

Large Chilean land package which is slated for

future joint ventures with senior mining companies. I expect to see a JV deal

before the end of the year.

Hot Chili Limited (HCH:ASX)

MCAP – $44 million (at the time of writing)

Cash – Over $1 million AUD (will need to finance for Phase 2

drilling)

Christian Easterday is Managing Director.

2 Projects: Cortadera Copper Porphyry Project

and Productora Copper Project.

Cortadera was optioned from a private Chilean

mining group, SCM Carola, earlier this year.

Located 14 km from Productora Copper Project.

Initial 5,500 m drill program was highlighted by

the discovery of a new high grade zone at Cuerpo 3, the main porphyry- CRP0013D

– 750 m grading 0.6% copper and 0.2 g/t gold from 204 m depth, including 188 m

grading 0.9% copper and 0.4 g/t gold.

Exploration potential – geochemistry and geophysics

(ground mag and IP) have identified a North Target area which has never been

drilled.

Exploration potential – Additionally, each of

the 4 porphyry centres remain open at depth and laterally.

Phase 2 drilling to commence shortly.

Maiden resource on Cortadera to be released very

soon.

Productora Copper Project

Total Proven and Probable Reserves (JORC) –

166.9 tonnes at 0.43% copper, 0.09 g/t gold and 138 ppm molybdenum (at metal

prices – Cu $3.00 USD/lbs, Au$1200 USD/oz and Mo $14.00 USD/lbs).

Altus Strategies (ALTS:TSXV)

MCAP – $16.9 million (at the time of writing)

Cash – roughly $1 million in cash and securities

CEO Steven Poulton leads a team of geologists

and mining engineers who have a history of success in the resource industry.

Altus team has a long history of success in

Africa.

Insider Ownership – CEO Steven Poulton owns

14.2%.

Strategic shareholders, which includes –

Exploration Capital Partners (2012 and 2014) combined 13.2%, and Euro Pacific

Gold Fund 3.8%.

18 projects, all located in Africa, encompassing

a wide range of precious and base metals.

Prospect generator business model.

Targeting greater than $10 million USD per annum

JV financed exploration expenditures.

9 projects in the “Joint Venture Ready” portion

of their development – precious and base metals.

Millrock Resources (MRO:TSXV)

MCAP – $8.3 million (at the time of writing)

Cash – Over $2 million in cash and securities

Greg Beischer is President and CEO.

Millrock is mainly focused on mineral

exploration within the Tintina Gold Province located in Alaska, but does have

additional project interests in BC and Mexico.

Prospect generator business model.

No joint venture partners at the moment, however,

this is likely to change in the weeks to come.

Currently, the Goodpaster Project is a focus for

the company, as they are targeting an extension to Northern Star’s Pogo mine.

Using CSAMT geophysics Millrock is targeting a

deep shear zone to the west of the existing mine. Key to this program is the

fact that they are using the same contractor as Northern Star did to complete

the work.

Completion of the program will either be

followed by a decision to drill or wait for a JV partner to fund the drilling

of the prospective target.

Mundoro Capital Inc.

MCAP – $8.67 million (at the time of writing)

Cash – $3 million (Q1-2019)

Teo Dechev is President and CEO.

Prospect Generator business model.

Exclusively in Eastern Europe, mainly Serbia and

Bulgaria.

JOGMEC JV – Currently in Phase 2 program –

geophysics, with drilling to follow in Q3 2019 – JOGMEC can attain 51% of the

project by spending $4 million USD in expenditures by March 2019 and purchase

up to 80% of the project with the delivering of a Feasibility Study.

Freeport JV – Currently in Phase 1 program –

Alteration mapping and geophysics, with drilling to possibly follow near the

end of Q4 2019 – Freeport can attain 51% of the project by spending $5 million

USD in expenditures by September 2021 and up to 75% of the project by solely

funding an additional $40 million in expenditures by 2026.

Timok Project is up for Joint Venture, but no

partner at the moment.

Strategic Alliance In Bulgaria with JOGMEC.

Large institutional holdings – 58%.

Ardea Resources (ARL:ASX)

MCAP – $59.44 AUD (at the time of writing)

Cash – $11.2 million AUD

Andrew Penkethman is the CEO.

Focused on both precious and base metals, with a

primary push towards nickel-cobalt.

Goongarnie Nickel Cobalt Project – PFS: 2.25

Mtpa, before tax NPV of $2.4 billion and IRR of 31%, CAPEX cost $918 million

USD, Pressure Acid Leach (PAL).

Large gold and nickel exploration land package

totalling 3500 square kilometers.

Possibility to spin out gold focused projects

and make Ardea solely a nickel company as we move into what may be a strong

nickel price environment in the years ahead.

Equinox Gold (EQX:TSXV)

MCAP -$843.6 million

Christian Milau is CEO and Executive Director.

Ross Beatty is a major shareholder, owing 12% of

the company.

Gold focused, with 3 advanced staged / mines in

Brazil and California, USA.

Aurizona Gold Mine poured its first gold in May

2019, 2019 production guidance is set at 75 to 90,000 oz Au at a AISC of $950

to 1,025/oz.

Mesquite Gold Mine – in production, YTD 2019 –

$70.8 million in revenue, 52K oz produced, $780/oz cost and a AISC of $907/oz.

Production guidance updated to 125 to 145K oz at an AISC of $930 to 980/oz.

Castle Mountain – 3.6 Moz Au reserves, 16 year

mine life, $763/oz avg LOM AISC – construction to begin second half of 2019.

Overal,l Equinox should produce 200 to 235K

ounces in 2019, with a goal of attaining production over 1 million ounces per

annum by 2023.

ISO Energy (ISO:TSXV)

MCAP – $49.9 million

Cash – $3 million

Craig Parry is the President and CEO.

Board of Directors is led by the Chairman Leigh

Curyer, who is the CEO of NexGen Energy. NexGen owns arguably the best

undeveloped uranium deposit in the world.

Team has the background to be successful in the

Athabasca Basin.

NexGen owns 53.4%, Cameco owns 5.4%, Orano owns

2.0% and Institutional owns 19.2% – doesn’t leave much in the public float.

Summer Drill Program – Hurricane Zone – 8 holes

into a 16 hole program on their Larocque East Project, which is located in the

eastern portion of the Athabasca Basin. Targets are hosted in

Sandstone/unconformity. Drill program is expected to cost $1.5 million, leaving

them with $1.5 million going into 2020.

3 other projects in their portfolio – Thorburn

Lake, Radio and North Thorburn.

CanAlaska Uranium (CVV:TSXV)

MCAP – $11.24 million (at the

time of writing)

Cash – roughly $1.0 million in

cash and cash equivalents (April 2019).

Peter Dasler is President and CEO.

Prospect generator business model.

3 main Projects: West McArthur, Cree East and NW

Manitoba.

West McArthur is a JV with Cameco – Targeting a

unconformity-basement uranium deposit.

Cree East has no JV partner – 9 target areas

across the property, possibility of both basement and sandstone hosted uranium

deposits.

NW Manitoba lies in close proximity to the

Saskatchewan border and is similar geologically to Rabbit Lake, Collins Bay and

Eagle Point Uranium mines which are within 90 km of the property.

Goviex Uranium (GXU:TSXV)

MCAP – $65.6 million (at the time of writing)

Cash – $2.8 million USD

Debt – $8.0 million USD

Daniel Major is the President and CEO.

3 uranium projects, all located in Africa –

Madaouela, Mutanga and Falea.

Flagship Madaouela Project is at the definitive

feasibility study stage of development. The Republic of Niger has signed a

definitive agreement to jointly develop the project.

After-tax NPV@8% – $340 million USD, IRR – 21.9%

at a uranium price of $70 USD/lbs.

Orano (formerly Areva) operates a uranium mine

in close proximity to Madaouela, which is reaching the end of its mine life.

“The State is to receive an additional working

interest of 10% in exchange for approximately US$14.5 million of claims due by

the Company to the State comprised of the final €7 million Madaouela I Mining

Permit acquisition payment and settlement of previously challenged three years

of area taxes (US$6.6 million) (collectively, the “Debt”) between the Company

and the State related to the Madaouela Project. The Company is to receive a

final, complete and unconditional release without reserves in respect of the

Debt, upon the transfer the additional working Interest.” ~ News

Release

The company is working at optimizing its

metallurgy and subsequently extract value from the other base metals that are

present – nickel, cobalt and molybdenum. Gravity separation and floatation

techniques are being tested for their ability to concentrate the metals

effectively. If successful, these advances have the potential to positively

affect the project’s economics.

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I have NO business relationship with any of the companies mentioned in this article. I am a shareholder of Aethon Minerals.

“Society does not get endlessly richer and more sophisticated. Periodically things collapse. It is not the end of the world. It is the end of an age.” ~ Rickards – The Road to Ruin – pg.297

Change is coming, I can feel it.

My sample size isn’t overly large, but in my life, I can’t

remember society being as polarized between left and right as it is today. It

isn’t just Canada and United States, either, it seems to be a good portion of

the world.

So, why does it matter? Well, in my view, the root of where

we are economically begins with the culture of the society. In this case, I’m

referring to western culture or, more specifically, the derivatives of western

culture which are found in Canada and the United States.

Western culture is of particular importance because its ebbs

and flows, presently, have such a profound effect on the entire world. In fact,

I would suggest that what I’m feeling is actually the degeneration of western

culture and, in effect, the fall of the global economy as we currently know it.

For all intents and purposes, the United States represents

the peak of western culture, as its rise to the world’s top power over the last

100 years has been predicated on all the ideals, mainly liberty and freedom,

which allow the free thinking individual to prosper.

Instead, today we are headed on a path toward destruction.

This path is one which is moving to remove the liberty and freedom of the

individual and increasingly to replace it with government oversight,

effectively removing an individual’s responsibility of choice.

In essence, the left and right are fighting to establish who

knows best for everyone else. This will ultimately end in the failure of the western

culture and, along with it, the collapse of the global economy in its current

form.

Much like the previous three, Aftermath doesn’t disappoint as it sets out a blueprint for wealth

preservation in the coming chaos.

Let’s take a closer look.

Aftermath – Seven Secrets of Wealth Preservation in the Coming Chaos

Much like Currency Wars, The Death of Money andThe Road to Ruin, in Aftermath Rickards uses both his experience and financial knowledge to outline his thesis for why a reset to the global monetary system is inevitable.

The chapters in Aftermath

are broken down into topics, the ramifications of which could individually

or collectively trigger the next global economic meltdown.

In my own words, here are the 7 topics that Rickards covers:

Tariffs and Trade Wars

Debt to GDP Ratio

Behaviour Economics

Passive Investing

Velocity of Money

Global Monetary Reset

Terminal Unit

Each of the topics is deserving of its own chapter, however,

I particularly enjoyed the information Rickards provides on the debt to GDP

ratio and behavioural economics. In my view, these 2 topics are of particular

importance because I think that, ultimately, a crisis in the global economy

will start with them.

Specifically, I believe quantitative easing (QE) and low

interest rates are to the market as drugs are to an addict. Therefore, pick your poison; more QE and low

interest rates that will lead to an overdose, or go cold turkey, which will

lead to the tremors and, most likely in this case, death. Either way, change is

on the horizon.

Debt to GDP Ratio

Currently, the United States debt to GDP ratio sits at

roughly 105%, a level which Rickards explains is considered by most economists

to be above the point of no return. Once an economy reaches these critical

levels, the growth of the economy is destroyed as any profits are directly fed

into servicing the debt.

Japan is a great example of the effects of a high debt to

GDP ratio, as the Japanese economy has been stagnant for multiple decades.

The obvious question then is, can’t the U.S. expand their

debt to GDP ratio to the extent of Japan and still avoid a crisis? The answer

is probably not; there would be a crisis of confidence before it reached the

levels of the Japanese economy.

“The U.S. debt to GDP ratio is approaching the point at which it cannot expand much farther without inducing a crisis of confidence” ~ Aftermath

Firstly, while Japan’s debt is much larger than its GDP, the

saving grace for the Japanese, in my opinion, is the fact that the Japanese

people are its largest holders of its debt. Because of this, I believe there is

a level of protection that the U.S., for example, doesn’t have.

Second, while the U.S. does appear, superficially, to have

room to grow its debt to GDP ratio, the potential lack of confidence in the

U.S.’s ability to service that debt begins to heighten. Unlike the Japanese, a

good portion of the U.S. debt is held overseas and, thus, presents a major

hurdle to further expansion.

Dwindling confidence will snowball and surely cause a major

economic crisis. America’s debt to GDP ratio is in risky territory. In the

chapter, ‘Putting out the Fire with Gasoline,’ Rickards walks you through the

history and risks associated with debt to GDP rations and, most importantly,

provides a tip for protecting your wealth against this major risk.

Human Behaviour

“Are humans risk adverse slugs or overconfident pretenders? The answer is both, depending on past circumstances and current conditions at the point of decision. This behaviour contradiction, one of many, illustrates why it is so difficult to make sense of human behaviour in markets” ~ Aftermath

We all have cognitive bias that affects the decisions we

make. More specifically to the basis of this book review, it is the bias-laden

investment decisions that many of us make that pose a major risk to the

economy.

In the investment world, there is a tendency to follow the

herd into buying the most popular stocks – for example, the FANG stocks

(Facebook, Apple, Netflix and Google) or using the most popular investment

techniques, such as passive or index investing. While the herd mentality can

sometimes provide short-term profits, over the long haul, it typically ends in

losses.

Currently, we sit at a very risky juncture in the stock

market, where it sits at all time highs. All time highs mixed with the hyper-synchronicity

investments is extremely dangerous for both the individual investor and the

market as a whole.

If or when losses begin to mount, it will have a contagion

effect on the market and, undoubtedly, lead to what could be major losses.

There is so much more to this topic which Rickards covers in

the book – I won’t spoil it. Understanding this one chapter in the book could make

all the difference in preserving your wealth.

Concluding Remarks

While it is easy to get caught up in the ‘when,’ as in when will

the crisis occur, it really is a waste of time. No one can predict when complex

events such as a global monetary reset will take place. In my opinion, it’s

important to continue to live life as you normally would, but with some added

financial prudence.

In my view, Aftermath is a MUST read for everyone, not just for those who are focused or

interested in the global economy. The

benefits of understanding the ramifications of what has happened in the global

economy over the last 10 years is integral for understanding where we may be

headed.

In Aftermath,

Rickards lays out the groundwork needed to protect your wealth in the future,

no matter what’s around the corner.

While it may not be imminent, it does appear to be inevitable that a global monetary reset is on the horizon. Read Aftermath, The Road to Ruin, The Death of Money and Currency Wars – you won’t regret it!