Author: admin

Premium Issue #1 – February 2020

Books – My Top 5 General and Resource Focused Favorites

Junior Resource Sector Investing: The Risks, Rules & Strategies You Need to Know

Fireweed Zinc – A Return to Market Darling in 2020?

Mr. Market never disappoints, the cycle between market darling and bottom dweller is continuous and really doesn’t discriminate – everyone is afflicted at some point. The key is to find the companies that are currently bottom dwellers, but truly deserve to be valued as market darlings.

More on this point, a few years ago, while attending a resource sector investment conference, I heard Rick Rule say, and I’m paraphrasing,

“In the short-term, the market is a voting machine and in the long-term, it’s a weighing machine.”

Rick Rule

In my view, Rule is saying that in the short term, Mr. Market is more emotional and swings with the popular vote, so to speak. In the long term, Mr. Market is more calculated and quantitative in its approach and, therefore, allows each company to attain their intrinsic value – good or bad.

Today, I have for you some comments on a sector and, more importantly, an investment thesis on a company which I believe is tremendously undervalued. The sector is zinc and the company is Fireweed Zinc.

Let’s take a look.

The Zinc Market

One of the hottest metals markets to be invested in over the last 5 years has been zinc. From its low in late 2015, to its high in early 2018, the zinc price more than doubled and, with it, brought a ton of attention to the junior zinc companies.

The zinc price strength was derived by supply constraints as a number of mines and smelter facilities closed or had their production suspended.

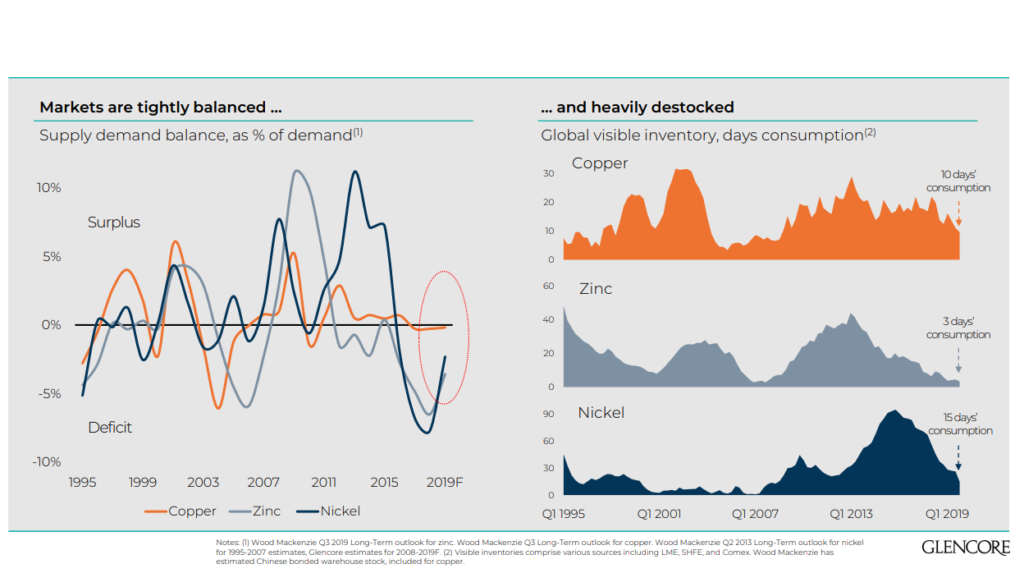

Glencore has a great graph, in their most recent corporate presentation, of the current global metal inventories of copper, zinc and nickel. All of which remain low, zinc in particular sits at 3 days of consumption – which, I think, many would equate with price strength, not weakness.

Today, however, the zinc price has fallen drastically from its highs above US$1.50/lbs and is sitting at roughly US$1/lbs.

This major fall in the zinc price has brought many of the junior zinc company share prices with it, and I believe it gives investors a great buying opportunity, if you choose wisely.

Fireweed Zinc (FWZ:TSXV)

MCAP – $20.7 million (at the time of writing)

Shares – 37.7 million

FD – 44.7 million (only a small amount of warrants outstanding)

Cash – roughly $1 million

Ownership – Management – 19%, TECK – 10%, Hudbay – 10%, RCF – 13%

NOTE: Teck was the lead order in the $5 million private placement early in 2019, purchasing 2.1 million shares for an investment of $1.75 million. Also, RCF topped up their position purchasing $750K worth of shares.

So why invest in Fireweed Zinc?

Besides a tight share structure and good strategic ownership, I think investment in Fireweed at its current MCAP comes down to 2 main points: its people and project.

Management

First and foremost, the investment thesis starts with CEO, Brandon Macdonald. Brandon is a geologist by trade and has a very good educational background with an MBA from Oxford. Now, I don’t personally know Brandon as well as I would like to, but I do have a couple of friends that know him very well and speak very highly of him – which is good enough for me.

Additionally, in my opinion, the fact that Brandon is from the Yukon or, more specifically, Ross River, I believe this is an X-Factor and something that will pay huge dividends in the future.

Another important factor in the Fireweed story is its association with Discovery Group. In fact, co-founder and principal at Discovery Group, John Robins, is the Executive Chairman and brings a history of success in the Yukon, ie. Kaminak Gold, and an extensive rolodex which opens doors to both capital and technical knowledge.

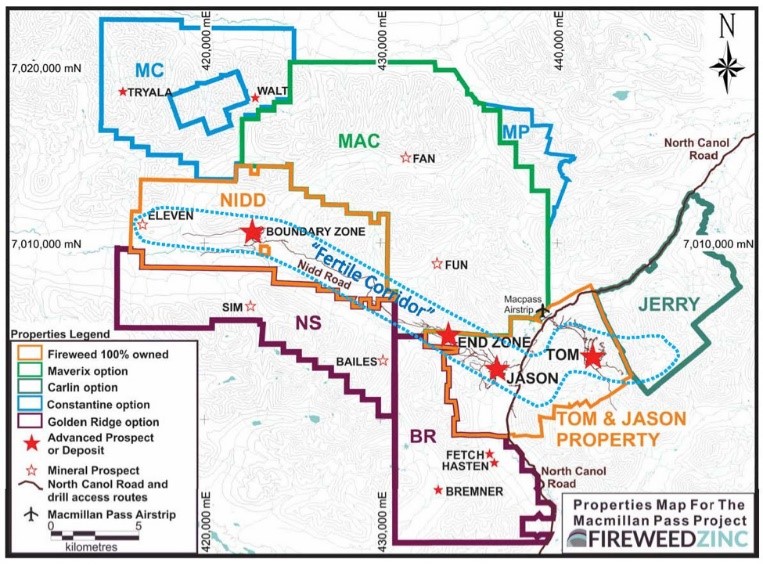

MacMillan Pass Project

I believe that Fireweed is undervalued considering the quality of its assets – MacMillan Pass Project. I say this, however, I must add the caveat that the MacMillan Pass Project is not economical at the current metal prices given their 2018 PEA.

To start, let’s take a look at the 2018 PEA figures for perspective:

After-tax NPV@ 8% – $1.1 billion

After-tax IRR of 24%

Pre-Production CAPEX – $404.3 million

Open Pit / Underground Mine

Mine Life – 18 years

Payback – 4 years

Indicated Resource – 11.2 Mt: Zinc 6.59% – 1.63 billion lbs, Lead 2.48% – 0.61 billion lbs, Silver 21.33 g/t – 7.69Moz , Zinc Eq. 9.61%

Inferred Resource – 39.5Mt: Zinc 5.84% – 5.08 billion lbs, Lead 3.14% – 2.73 billion lbs, Silver 38.15 g/t – 48.41 Moz, Zinc Eq. 10.0%

Assumed metal prices – Zinc US$1.21/lbs, Lead US$0.98, Silver US$16.80/oz

These are some great numbers and really separate the MacMillan Pass Project from the rest of the pack of other undeveloped zinc projects worldwide.

It starts with the size of the Tom and Jason deposits, which have a combined indicated and inferred resource of over 50 Mt.

The impact of having such a large resource has a trickle-down effect on the rest of the important aspects of the project and, most importantly, I think, allows for a long mine life, giving a would-be buyer the chance to be right about the economic viability of the project over its lifetime.

One of the issues of a shorter mine life is that they have to be developed at the proper time or they risk being ready or in production, over the majority of their life, during a metal price environment which is uneconomic.

There are a couple of size comparisons for Fireweed, but each is valued much higher by the market. Now, not every pound or ounce of metal is created equal, I totally agree. In this case, however, I think the market has it wrong.

Silver Credit

If you do your research on the undeveloped zinc companies worldwide, you will find that a large portion have completed economic studies using a zinc price between US$1.20 and US$1.30 per pound.

Therefore, you need to chose right if you’re going to invest in a zinc company, because when the zinc market does eventually come back, it’s going to be the best projects out of that grouping which are going to be acquired or developed.

So what’s going to separate the wheat from the chaff?

It could be a number of different things, from jurisdiction to upfront capital cost, to acquisition cost, to economics. The location of each project can’t be changed and, therefore, I think the best companies will separate themselves by continuing to improve their projects, by increasing NPV / IRR and, ultimately, trying to reduce the metal prices that they require for an adequate return on capital invested.

Personally, I think that zinc companies that have a silver component to their deposit stand a good chance of standing out from their peers given the outlook for precious metals in 2020.

Now, I won’t be hanging my hat on this for the basis of my investment; speculating in metal price movements is not a good reason to buy a junior resource company.

Fireweed, however, does have close to 60 Moz of silver, which is large and fairly rare if you look around the junior resource space. High silver prices could be icing on the cake to the Fireweed investment thesis, if it were to head above US$20/oz.

Boundary Zone Drilling

Thus far, all of the information regarding MacMillan has been with reference to the Tom and Jason Deposits. Another ace up CEO MacDonald’s sleeve, however, could come from the Boundary Zone.

Over the last couple of months, I have been pleasantly surprised with the drill results that have come from the Boundary Zone. They are highlighted by:

- Hole NB19-002 – 230m estimated true width of 4.14% zinc, 0.3% lead and 9.7 g/t silver (WOW!)

- including interval 8 to 150.30m – 100m estimated true width of 7.94% Zn, 0.1% Pb, 11.1 g/t Ag

- including 27.80 to 40.10m – 8.7m estimated true width of 9.2% Zn, 0.04% Pb, 11.5 g/t Ag

- including 115.81 to 127.0m – 7.9m estimated true width of 17.47% Zn, 0.08% Pb, 36.0 g/t Ag

- including 120.64 to 127.0m – 4.5m estimated true width of 28.72%, 0.13% Pb, 59.9 g/t Ag

- including 139.35 to 148.42m – 6.4m estimated true width of 42.49% Zn, 0.75% Pb, 42.1 g/t Ag

- 145.65 to 146.53m – 0.6m estimated true width of >60% Zn, 0.2% Pb, 61.2 g/t Ag

- including interval 8 to 150.30m – 100m estimated true width of 7.94% Zn, 0.1% Pb, 11.1 g/t Ag

- Hole NB10-001 – 250m estimated true width of 3.44% zinc, 0.1% lead and 5.6 g/t silver

- 93.69 to 117.0m – 23.31m of 16.35% Zn, 0.09% Pb, 27.9 g/t Ag

- 93.69 to 98.54m – 4.85m of 31.96% Zn, 0.14% Pb, 39.8 g/t Ag

- 94.84 to 95.85m – 1.01m of 47.70% Zn, 0.21% Pb, 50.2 g/t Ag

- 111.40 to 117.0m – 5.6m of 29.19% Zn, 0.2% Pb, 62.8 g/t Ag

- 113.54 to 117.0m – 3.46m of 36.36% Zn, 0.29% Pb, 81.2 g/t Ag

- 93.69 to 98.54m – 4.85m of 31.96% Zn, 0.14% Pb, 39.8 g/t Ag

- 226.20 to 238.05m – 11.85m of 9.18% Zn, 4.45% Pb, 71.6 g/t Ag

- 230.30 to 236.0m – 5.70m of 12.16% Zn, 7.09% Pb, 71.6 g/t Ag

- 230.30 to 233.22m – 2.92m of 18.96% Zn, 3.02% Pb, 75.1 g/t Ag

- 233.88 to 236.0m – 2.12m of 5.74% Zn, 14.26% Pb, 180.9 g/t Ag

- 230.30 to 236.0m – 5.70m of 12.16% Zn, 7.09% Pb, 71.6 g/t Ag

- 93.69 to 117.0m – 23.31m of 16.35% Zn, 0.09% Pb, 27.9 g/t Ag

These are great results and near surface to boot. The Boundary Zone has the potential to be a real difference maker in the size and production profile of MacMillan, moving forward.

Additionally, the company is testing XRF ore sorting technology, which would, theoretically, be used in conjunction with the mining of the Boundary Zone, thus feeding the mill with high grade ore, in-conjunction with that which is being produced from Tom and Jason.

Unlike metal price predictions, I will speculate that this is going to improve the NPV of the MacMillan project and, therefore, is a big part of the investment thesis in Fireweed.

Concluding Remarks

In many cases, junior resource companies have a period in which they proverbially fall from grace in the eyes of the market. In many cases, it’s warranted, as the company eventually reaches its intrinsic value of 0. In special cases, however, value investors can find a diamond in the rough.

In my opinion, Fireweed Zinc at its current MCAP is a diamond in the rough and is why I recently bought shares.

Now an investment in Fireweed isn’t without risk.

The first risk is Fireweed’s cash position. Currently, they have roughly $1 million, which is not enough to do anything highly impactful. Dilution at such a low MCAP is not ideal, but may be necessary. Personally, I would like to see Teck and RCF be lead orders in the next placement in 2020.

The second risk is the zinc price; further weakness in the price could put Fireweed into neutral. As I mentioned earlier, however, almost the whole undeveloped zinc market would be in the same boat and, therefore, I’m happy to stick with the best undervalued issuer.

Finally, I think it’s justified to be skeptical on the Yukon. It’s a great jurisdiction in many respects and there has been success with Victoria Gold now a producing gold mine. But, a large primary base metal project is a different beast altogether.

In the end, I think that MacMillan has the right location in terms of accessibility to make it work and, therefore, I think the risk is noted, but not detrimental to its development.

NOTE: See BMC Minerals, who are in the final stages of permitting their primary zinc project, which is located in close proximity to the MacMillan Pass Project.

In closing, I’m a buyer and am bullish on Fireweed.

First, because of the people. Brandon Macdonald is a smart and trustworthy man, who is at the very beginning of what I think will be a long and successful career in the mining industry.

Moreover, he is supported directly by an Executive Chairman, John Robins, who has a stellar resume from his more than 35 years in the business.

Second, I believe the MacMillan Pass project is in a class of its own, especially given its current valuation. It’s a large deposit, and given the success with step out drilling at the Tom deposit, and arguably more importantly, the great results from the Boundary Zone, I think it’s about to get a whole lot better in the future.

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I have NO business relationship with Fireweed Zinc or any other company mentioned in this article. I do own shares in Fireweed Zinc.

Nevada Site Visits – Day 2 – U.S. Gold Corp.

Have we reached peak gold?

I have read this headline multiple times, but never really listened to the commentary. Now, this isn’t for any specific reason, it’s just that, generally speaking, I really don’t read or listen to much sector commentary.

To start, I think it’s really important to define what exactly peak gold is before discussing it.

Personally, when I think of peak gold, it is a scenario whereby global production and discovery never again reaches the highs of the past; essentially, it’s all downhill from here.

To start, does it matter if this is true?

In my mind, it’s debatable, as gold is very different from almost every other metal. Essentially, all the gold that has ever been mined still exists – it isn’t consumed in the traditional sense.

Bullishness on gold based on supply and demand, therefore, is hard for me to accept because supply is readily available to come into the market at any time.

My thought is that peak gold or, really, peak anything, is just a matter of price.

Price or economics is the ultimate motivator; as we have continually seen throughout history, it pushes innovation.

Oil is a great example.

During the years of +$US100 per barrel, much of the narrative focused on peak oil, which coincidently sounds a lot like what we are hearing about peak gold now.

We are finding less, we have to go deeper and explore in more remote jurisdictions or harsher environments, making it more expensive to extract – we have hit peak oil.

Wrong, high oil prices spurred the innovation of horizontal drilling and, of course, have broadened the discussion on other fuel sources.

Each metal is going to be different, I agree. However, generally speaking, my thought remains that scarcity leads to higher prices and higher prices lead to innovation and/or substitution.

In gold’s case, I think we’re going to see the industry innovate itself in exploration and mineral processing.

Firstly, with regards to exploration, I think it will be geophysics that sees a major revelation in the future.

Pre-drilling exploration work is becoming more and more important in identifying and prioritizing targets and I believe this is where we may see the bulk of innovation.

Second, there’s a large portion of known deposits with refractory gold. It’s my guess that money will be spent to optimize the mineral processing techniques that are needed to liberate this trapped gold.

As the gold price rises, more and more attention will be given to producing and discovering it – ergo a new renaissance will emerge and gold’s horizontal drilling equivalent will be born.

Or, maybe not. Time will tell!

Today, I have for you my notes from the field from day 2 of my Nevada site visit tour. U.S. Gold Corp was the focus of the second half of the trip and took us to the northeastern portion of the state, near Elko.

Let’s take a look.

U.S. Gold Corp (USAU:NASDAQ)

MCAP – US$18.2 million (at the time of writing)

Shares – 23.6 million

FD – 29.9 million

Cash – roughly $2 million

NOTE: On June 20, 2019 U.S. Gold Corp closed a $2.5 million F Series convertible preferred stock in a non-brokered registered direct offering.

NOTE: U.S. Gold Corp was acquired by Dataram in mid-2016. At the time, U.S. Gold Corp. was in possession of a PEA level Copper King project located in Wyoming. Keystone project acquired after formation of the new company.

Keystone Project

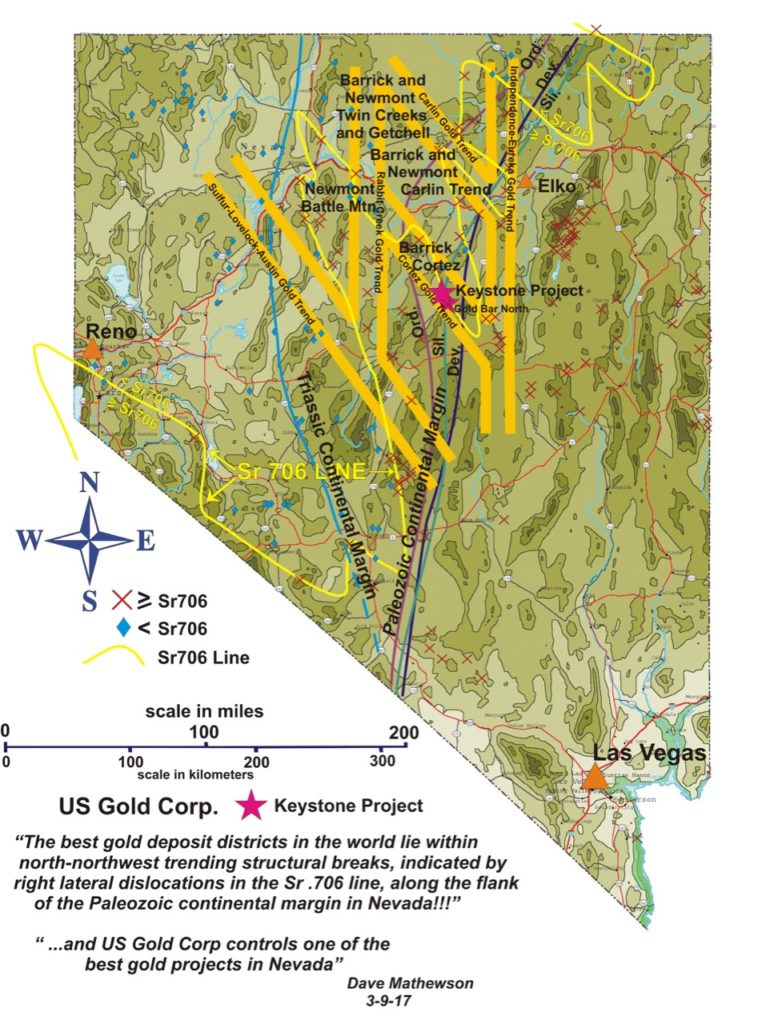

U.S. Gold Corp.’s flagship Keystone project is located on the Cortez Trend, just south of Nevada Gold Mines’ Cortez Hill mine.

NOTE: Nevada Gold Mines was formed through the merger of Barrick Gold’s and Newmont Goldcorp’s Nevada assets.

Keystone, in its current form, represents the consolidation of what used to be a few different properties and, in total, encompasses 20 square miles or roughly 5200 hectares.

Past operators of these various claim blocks were Newmont, Chevron, USMX, Placer Dome and McEwen Mining Co.

Note: Dating back to the 1980s, a total of 240 shallow, less than 100m deep, drill holes have been drilled on the various portions of the property.

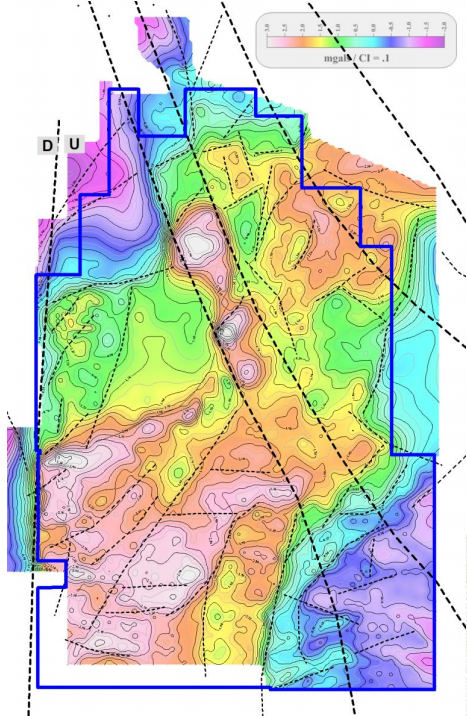

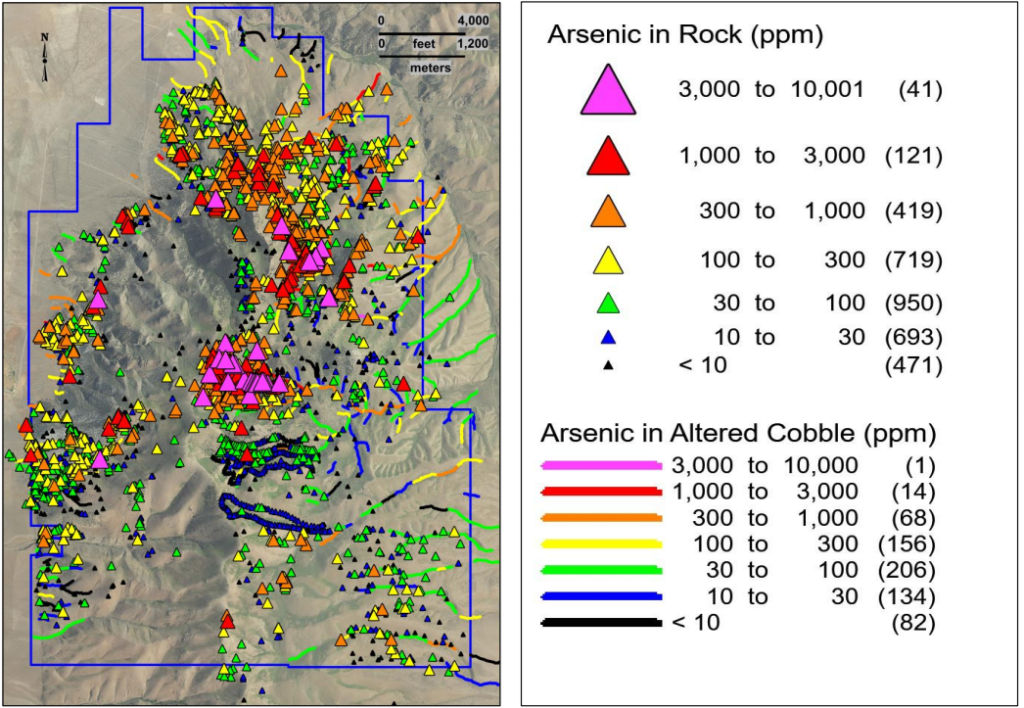

Geochemical and Geophysical Data

Keystone’s geochemical database consists of 7,372 soil samples, 3,414 rock samples, 666 fine-sediment stream samples and 661 altered stream cobble samples.

Along with the strong database of geochemical data, they have also completed regional magnetics on the project.

As the image demonstrates, the magnetics are interpreted to reveal a northwest striking structure. These structures have been confirmed by geological mapping and through geochemical testing.

For example, most of the soil sampling data reveals high concentrations of pathfinder metals within this northwest trend.

The arsenic samples in particular provide us with a clear visual concentration along the northwest trend, and also appear to follow a secondary structure to the southwest.

More data can be found within the Keystone specific page, too – geochemical testing, magnetic report, Keystone Master of Science Thesis, etc.

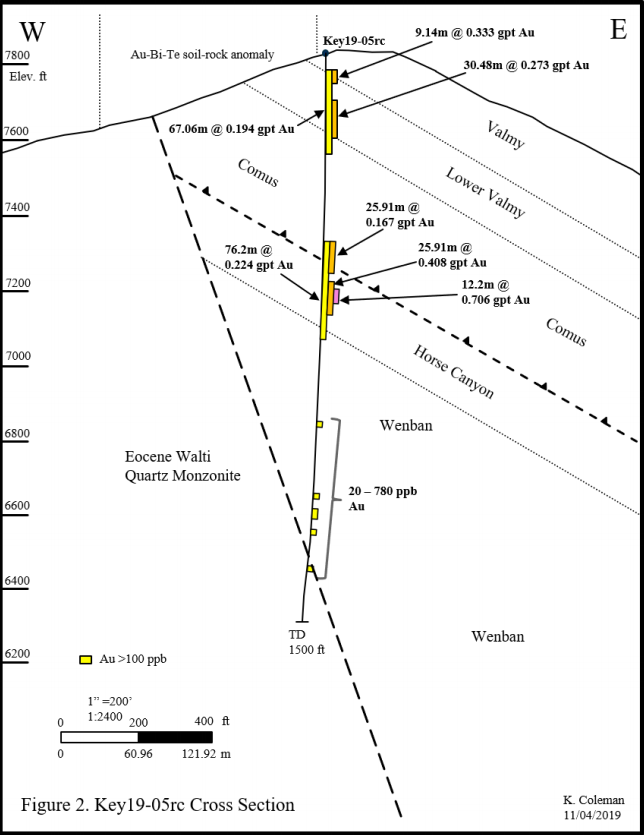

2019 Drill Program

The 2019 drill program consisted of 7 holes, 6 RC and 1 diamond, totalling 4,000m. The first hole of the program was a follow up on hole 18-09rc, in Sophia Target Zone, from the 2018 program, which encountered over 350m of nearly continuous oxidized breccias, but was lost approximately 1600ft or 500m down hole, due to hitting a 20ft void.

CEO, Ed Karr, explained to me that they were very interested to follow up on this lost hole because of its possible similarities to Nevada Gold Mine’s Gold Rush deposit.

Gold Rush is a deep deposit, with voids or a Swiss cheese like matrix of rock above it. Hence, their excitement. Unfortunately, the follow up hole was a dud, returning mostly clay.

The 6 remaining holes, all RC, were drilled within the Tip Top, Sophia South and Nina Skarn Target Zones.

To date, U.S. Gold Corp. has really had no significant gold intercepts to list, but have shown many intersections with anomalous gold, which they define as greater than 10ppb gold over 50ft thick.

The 2019 drill program continued with similar results, mainly low grade gold over thin widths, except for hole 19-05rc which was drilled within the Nina Skarn Target Zone.

19-05rc intercepted 67.06m of 0.194 g/t gold, which includes intervals of 9.14m of 0.333 g/t gold and 30.48m of 0.273 g/t gold.

Additionally, further down hole, it intercepted 76.2m of 0.224 g/t gold, which includes 25.91m of 0.167 g/t and 25.91m of 0.408 g/t gold, which includes 12.2m of 0.706 g/t gold.

Now, these aren’t high grade hits by any means, but compared to historical results and the bigger geological picture, they may indicate the presence of a larger gold system.

Karr explained that they believe this mineralization is a part of a halo surrounding what could be a larger, higher grade gold deposit northeast of drill hole 19-05rc. U.S. Gold Corp.’s geologists believe that it’s an intrusion in this northeast area of the property which may have acted as the heat engine for the mineralization intercepted in this hole.

This area between hole 19-05rc and the northeast intrusion will be the main focus of the company’s next drill program, as they try to vector in on what they hope is a high grade gold deposit.

While they have narrowed their exploration focus on Keystone, in my opinion, it’s still akin to finding a needle in a haystack – 2020 drilling at Keystone should be interesting.

Winter is upon them in this mid portion of the Battle Mtn – Eureka / Cortez Trend, and given the mountainous terrain, they will not be able to get drills back into Keystone until next spring.

To add, with roughly $2 million in cash left, U.S. Gold Corp will have to raise more money before conducting next year’s program.

Copper King

The Copper King project is 100% owned by U.S. Gold Corp. and is located in southeastern Wyoming, approximately 32 km west of the city of Cheyenne.

An updated version of the PEA was completed for U.S. Gold Corp. in 2017 and can be found here.

In my discussion with Karr, he indicated that they are working on a PFS for the project and expect it to be complete by mid-year.

Personally, I’m interested in seeing the mineral processing results, as they will have to use a wider range of samples in their testing, as the PEA met work mainly used high grade material from the centre of the deposit.

Here are the high level highlights from the 2017 PEA:

Gold Price Assumption – US$1275

Copper Price Assumption – US$2.80

Pre-tax NPV@5% – $178.5 million

Pre-tax IRR – 33.1%

CAPEX – $113.66 million

Measured Resource – 13.7 Mt at 0.62 g/t Au (272K oz) and 0.198% Cu (60.1 mlbs)

Indicated Resource – 40.4 Mt at 0.48 g/t Au (654K oz) and 0.182% Cu (162.8 mlbs)

Inferred Resource – 14.1 Mt at 0.38 g/t Au (174K oz) and 0.2% Cu (62.5 mlbs)

Concluding Remarks

Currently, U.S. Gold Corp. has a MCAP of around $25 million CAD and, in my opinion, makes it fairly valued given their assets.

In my view, the bulk of U.S. Gold Corp.’s value is found within their PEA level Copper King project, where I’m happy to hear they are moving forward with PFS level development work.

On the other hand, while the Keystone project has the right address, the visual hallmarks of a prospective Carlin style gold project, it just hasn’t produced the results for me to give it much value.

In saying this, hole 19-05rc may end up being the key needed to discover Keystone’s yet to be found gold deposit. More time and money is going to be needed to move this forward and prove their current thesis.

As an investor in the junior resource sector, I have learned that it’s integral to protect my downside risk and, therefore, I’m always looking to put my money into companies that are selling for less than their intrinsic value.

As I said, I believe at its current MCAP, U.S. Gold Corp. is arguably selling for its intrinsic value and, therefore, makes it less appealing to me considering the money and upcoming catalysts needed for share price appreciation.

I’m not a buyer of U.S. Gold Corp., but will be adding it to my watchlist, as tax loss season is upon us and who knows where the market may be headed.

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I have NO business relationship with any of the companies discussed in this article, however, U.S. Gold Corp. did pay for my site visit expenses. I do NOT own shares in U.S. Gold Corp.

Nevada Site Visits – Day 1 – Silver One Resources

Does successful investing within the junior resource sector start with choosing the right metal?

I’ve said it many times, I believe speculating in the direction of a metal price is essentially impossible to do with any consistency, and shouldn’t be the reason for investing in a junior resource company.

This statement is more controversial than I had imagined and has been challenged many times over the last 3 or 4 months.

Let’s use the gold price as an example. The narrative surrounding higher gold prices can take many forms, but for most people, a higher future gold price is driven by the instability of the global financial system, which has been propped up by quantitative easing and low interest rates throughout the world.

I have no issue with that argument.

However, from 2011 to 2015, the gold price was almost cut in half and, as we all know as junior resource sector investors, besides the 8 month blip in 2016, the juniors, on a whole, have been in a bear market since 2012.

So why the precipitous fall from grace?

- Must have been the miraculous repair of the global financial system.

Not a chance. In my opinion, the global financial system has only worsened over the last 8 years. Countries are more in debt than ever and interest rates continue to be near record lows.

- So, it must be gold supply manipulation by the world’s central banks.

Maybe, but honestly, I find it very hard to accept any thesis on gold supply and demand considering that, essentially, all the gold ever mined still exists.

- US$1900/oz was too high, the market over valued the amount of risk in the global market.

I’m not sure I have heard anyone use that argument to explain the fall in the gold price, but I think that there is some sensibility to it. Personally, though, given where we are today, I think we will see the gold price break US$2000/oz.

When? Great question! I have no idea and there-in lies one of the main issues with metal price speculation.

In reality, given a long enough timeframe, you can be right about the direction of the metal price, however, given the time value of money, are you actually right?

My point with this example is to show that while the popular narrative and the fundamentals of a metal appear to be pointing to a rising metal price, global markets are complex and hard to predict.

Thus, it’s my opinion that especially for the average investor, there’s very little value in trying to guess or follow someone who believes that they can predict the direction of a metal price.

If you’re bullish on the metal, buy the metal – it doesn’t come with the risk associated with the miners, who can lose you money due to a variety of factors that include exploration failure, poor metallurgy or political strife.

Successful investing in junior resource companies is predicated on 3 main criteria: Invest in the best people, protect your downside risk, and be a deep thinker – see through the popular narrative.

Today, I have for you the details from Day 1 of my Nevada Site Visit Tour, where I had the chance to visit Silver One Resource’s flagship Candelaria Project, which is located in the northwestern portion of Nevada, near Hawthorne.

Let’s take a closer look.

Reno, Nevada

On October 28,th I caught the 6:20am flight out of Toronto to Denver and hopped on a connecting flight which brought me to Reno, Nevada before noon Pacific time.

Unless you’re travelling to Las Vegas, in my experience, Nevada is always multiple flights from the east coast. It’s even worse if you’re flying into Elko, Nevada, which is located in the northeastern portion of the state – it’s been a marathon 3 flights the last 3 times I’ve taken the trip.

Flights aside, I really enjoy this part of the United States. The air is fresh and clear and once you leave the cities and begin to travel into the smaller towns, it’s like going back in time from a number of perspectives.

After landing in Reno, we made the 3ish hour drive south to Hawthorne, where we spent the night. The next morning, it was a short drive to Candelaria and a good review of what Silver One is planning at its flagship asset.

Source: Technical Report

Hawthorne sits directly south of Walker Lake and, interestingly, is home to the world’s largest ammunition depot. The depot covers 147,000 acres and has over 600,000 square feet of storage space within 2,427 bunkers.

Unfortunately, I don’t have a picture to share. You will have to trust me when I say that it’s an amazing sight to see and really confusing if you don’t know what you’re looking at.

Besides being home to the world’s largest ammo depot, Hawthorne is home to 3,000 people.

At our hotel, at least half of the guests looked to be with the mining industry in some shape or form. The other half were older couples, whom I’m sure were using Hawthorne’s Travel Lodge as a stopover on their way to Las Vegas.

Silver One Resources (SVE:TSXV)

MCAP – $44.79 million (at the time of writing)

Shares – 149.3 million

FD – 187.1 million

Strategic Shareholders – Eric Sprott 10.8%, SSR Mining 6%, Insiders 5.5%, First Mining Gold 3.4%

NOTE: Silver One closed a $4.976 million financing at a share price of $0.125 and a 3 year – ½ warrant at $0.20 on July 11, 2019. The PP shares will be free trading very soon and there’s a chance that some buyers may sell their shares and hold the warrants moving forward – FYI.

Candelaria Project

NOTE: Silver One has 1 remaining $1 million option payment on Candelaria, which is due in January 2020 to Silver Standard. Additionally, under the option agreement, Silver One must assume a $2 million reclamation bond relating to the historic heap leach pads at Candelaria. Instead of coinciding with the last option payment, this will be deferred until January 2023.

Being a past producing mine site, the Candelaria project has great infrastructure. It begins with close proximity to the interstate and a paved road right up to the main gates of the project.

Turning off the interstate, power lines follow you up and into Candelaria, with the sub-station sitting right next to a steel building. This is where Silver One is currently holding samples and other exploration equipment.

Additionally, Candelaria has access to water via wells that produce 500 to 600 gpm, I’m told, and sit in the southern portion of the property.

NOTE: From 1980 to 1999, the Candelaria mine produced 47 million ounces of silver before being closed due to low silver prices.

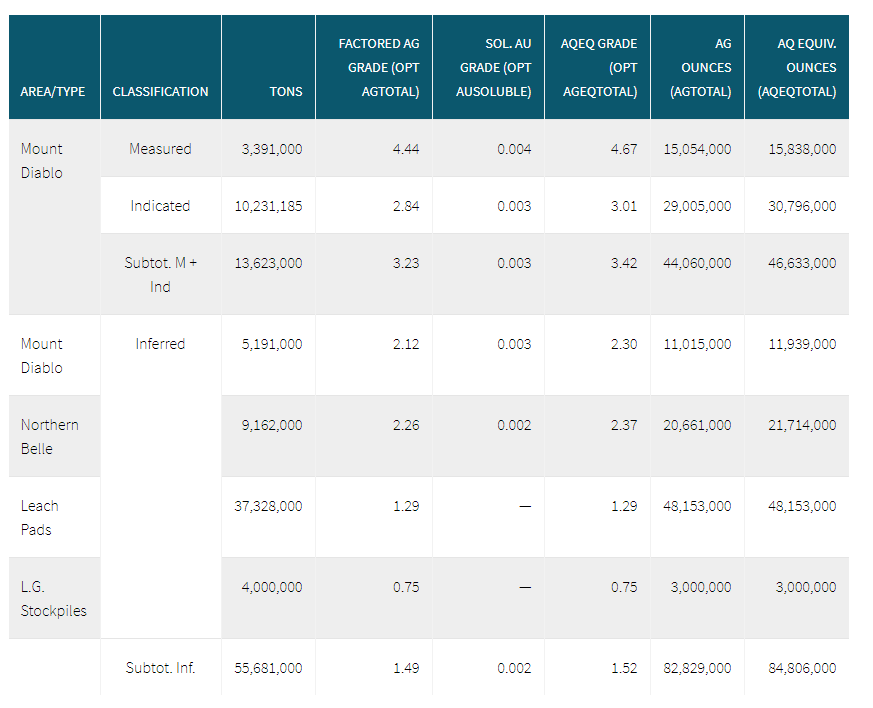

Historical Resource

The Candelaria project has no 43-101 compliant resources on any of its heap leach pads or deposits – Northern Belle, Mount Diablo, Lucky Hill Mine or Georgine Pit.

Thus, the historical resource table which I have included for your reference should be taken with a grain of salt.

HISTORICAL RESOURCE – NOT 43-101 Compliant

Silver One’s CEO, Greg Crowe, who led much of the discussion during the site visit, mentioned that an updated resource was a priority for the company moving forward.

In fact, most of the drilling this fall will be used to produce a 43-101 compliant resource.

Metallurgy

In terms of priorities, next to setting a base number for Candelaria’s resource estimate, the company will also focus a lot of attention on the project’s metallurgy.

As it stands right now, roughly 30% of Candelaria’s silver is non-recoverable through coarse grinding and cyanide leaching.

Preliminary mineralogical testing suggests that most of this non-recoverable silver is held within jarosite.

Having 30% of your resource non -recoverable is significant and, thus, is why it’s a priority for Silver One to improve.

NOTE: Initial metallurgical results show that 56% of the silver on the heap leach pads is cyanide soluble, leaving 44% in the non-recoverable category.

In my view, the metallurgical work represents biggest opportunity for the company. How or where else can they add that many payable ounces within a year for what is a fraction of the cost and risk of drilling.

Crowe explained that they are focused on finding the optimal milling (grinding) size needed to liberate the silver from the jarosite.

Of course, the amount of milling has to be balanced with the economics of the whole process. It’s one thing to liberate all the silver out of the jarosite, but if you need $50 silver to do it, is it worth it?

It will be very interesting to watch for these results, and much like the resource estimate, see what silver price is needed for this to be economic.

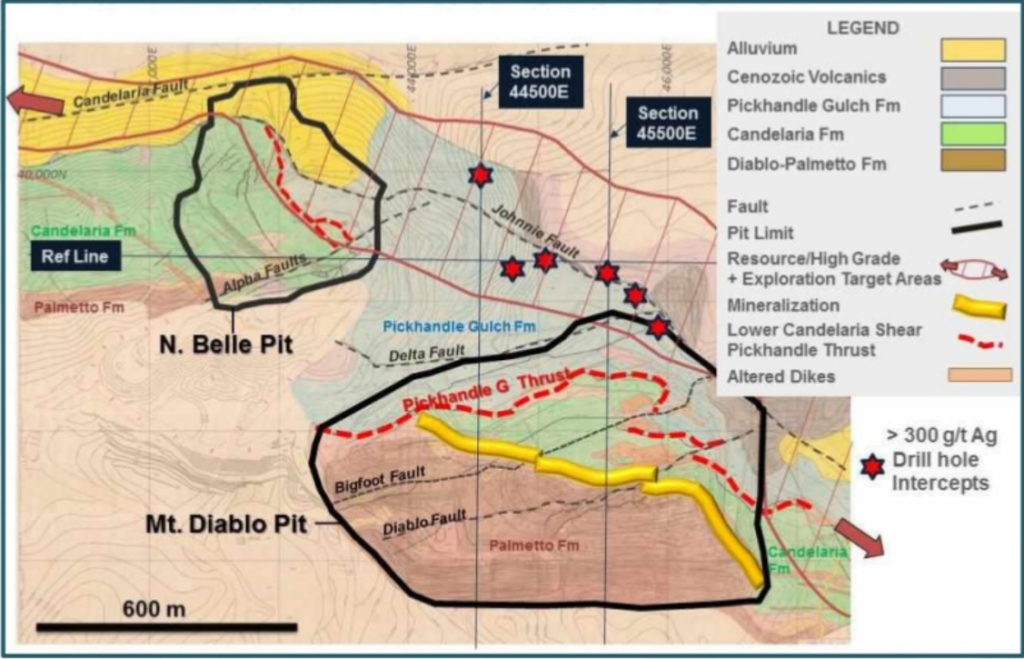

Drill Targets

Next to the Candelaria’s priority work, the resource estimate and metallurgical testing, there are some interesting exploration drill targets across the entire property.

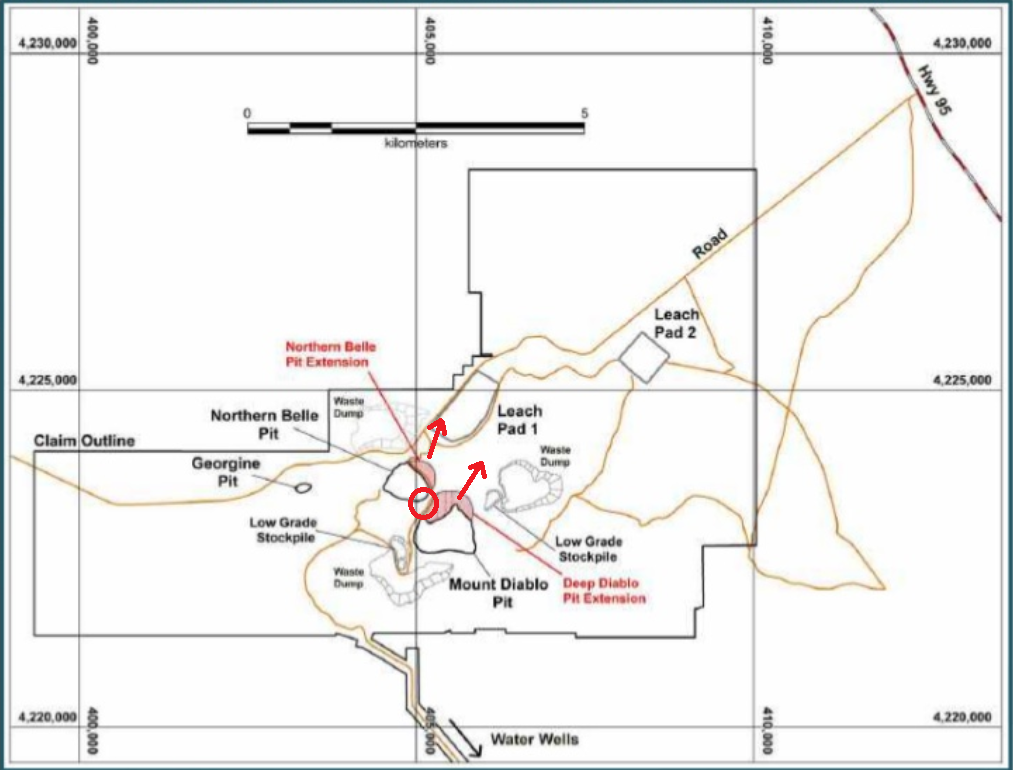

I will draw your attention to the image above, which gives us a top view of the project.

The Northern Belle and Mount Diablo pits are labelled and sit on either side of the red circle.

The first 2 targets are the most obvious. Silver One will be drill for down dip extensions, which I have represented using red arrows, on both pits.

Second, both deposits will be drilled for lateral extensions, specifically in between the 2 pits to see if they connect. Represented as the area within the red circle.

Historic Silver Standard Drilling

Historically, Silver Standard did hit silver mineralization in a number of holes in between the 2 pits, represented as stars in the image above.

Georgine Pit

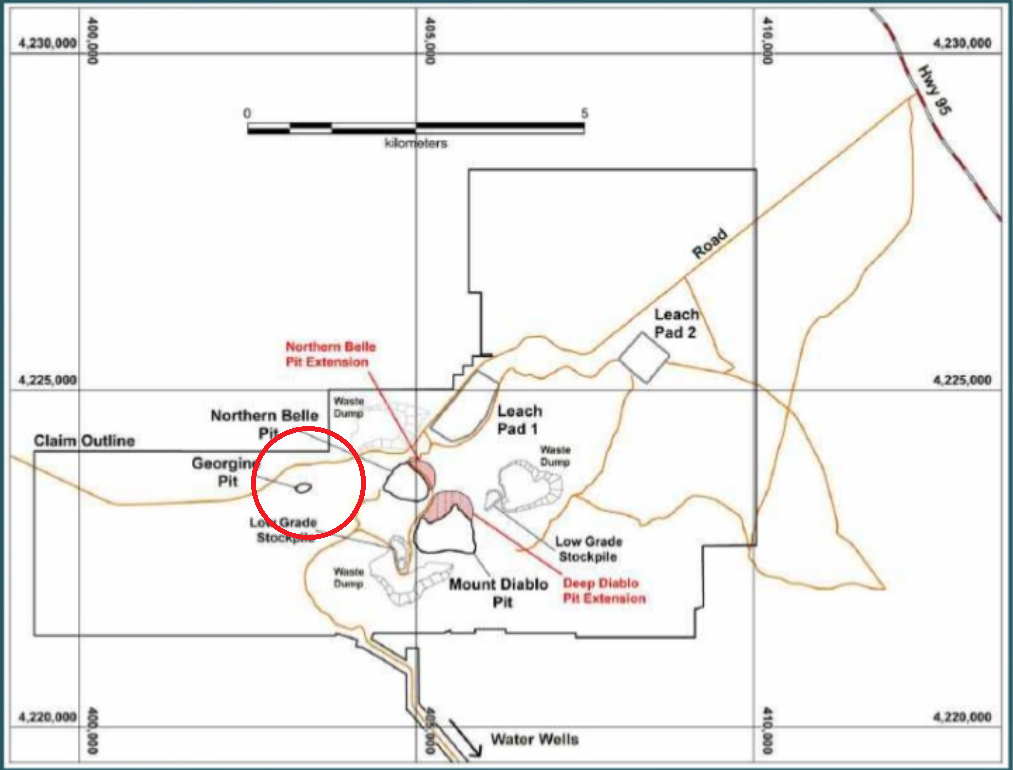

Now let’s take a look at the more abstract exploration targets at Candelaria.

In the image above, I have circled the next most prospective area within Candelaria.

This region of the property is interesting as it either represents a parallel or off-set mineralized structure to that which hosts Northern Belle and Diablo.

Currently, there are 2 known past producing pits in this area – Georgine and the Lucky Mine. Both are small, but when mixed with the magnetic anomaly the company has identified, could represent a much bigger system.

I couldn’t find a picture, but Crowe mentioned that the magnetic anomaly lies just north of the Georgine pit. Given this, they subsequently staked more ground along the north claim boundary you see in the image above. The new claim block represents an area of approximately 8 square kilometres.

Another interesting note on this area is the grab samples they have found. Crowe showed us one of the high grade copper, low grade gold samples they found in the immediate area surrounding Georgine.

Sample found near Georgine Pit

Crowe speculated about the possibility of there being an Iron Oxide Copper Gold (IOCG) deposit in this area.

They plan to follow up the grab sample with an IP survey, which could shed some light on any concentrations of sulphide mineralization in the area.

Concluding Remarks

It was a good site visit to Silver One’s Candelaria project, I believe I have a good understanding of where the company is and where they are headed.

I look forward to seeing the initial drill results from the company, which I am sure we will see before the end of the year. Additionally, more geophysical work on the new claim block and area surrounding Georgine pit should be really revealing to what may be there.

I, however, am not a buyer of Silver One Resources at this point; as there are a number of questions I have yet to answer.

First, will there be an onslaught of selling as this summer’s private placement shares become free trading?

Second, the metallurgical work is a HUGE part of this story and, really, I think, will be the main factor in classifying it as a good or great project.

Silver One has been added to my watchlist, as I eagerly await drill and preliminary met work results.

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I have NO business relationship with any of the companies discussed in this article, however, Silver One Resources did pay for my site visit expenses. I do NOT own shares in Silver One Resources.

O3 Mining – The 3rd Iteration of the Osisko Mining Group

“The desire for more, the fear of missing out, the tendency to compare against others, the influence of the crowd and the dream of the sure thing-these factors are near-universal. Thus they have a profound collective impact on most investors and most markets. The result is mistakes, and those mistakes are frequent, wide-spread and recurring. “ ~ The Most Important Thing Illuminated pg.97

Success in the junior resource sector is predicated on a few key things.

First and foremost, it’s vital to invest your money with the right people. The wrong people have the capability of destroying any semblance of value in a good project.

Second, you need to protect your downside risk as it pertains to a company’s share price versus its intrinsic value.

Finally, you need to be a deep thinker and see through the narrative of the herd. This point is as much about brains as it is about courage – it’s rare to have both.

Today, in mid-October, at the highest precious metals prices we have seen in 6 years, the junior resource sector is, for the most part, selling off.

It begs the question, why?

Is it profit-taking? Maybe for a few of the best names, but for the most part, I think many companies haven’t seen much of an uptick in their share price, even with the spike in metal prices over the last 3 months.

Is it premature tax-loss selling? I don’t think that’s totally out of the question.

Is it the narrative surrounding a large correction in precious metals prices, which has caused many to anticipate the fall in prices and sell?

Social media is a powerful tool, it wouldn’t surprise me if those calling for a correction are influencing a percentage of investors. There’s comfort in following the herd.

Or, is it a lack of confidence in high precious metals prices in the future? I think that makes a lot of sense.

Human behaviour suggests that most people project their immediate past into the future. I can, therefore, see a high percentage of investors expecting to see the gold price fall, which ultimately would lead to them incurring losses on the companies within their portfolio.

In the end, it’s probably the confluence of all of these points and many more which have caused there to be more sellers than buyers, at this point.

For me, I see it as an opportunity to add to my positions in companies already in my portfolio or buy tranches in new companies in which I have been waiting for weakness.

Today, I have some thoughts on a company that I believe has all of the right ingredients for success and, in my opinion, is selling at a discount to their intrinsic value.

The company is O3 Mining, the 3rd iteration from the Osisko mining group.

Let’s take a look!

O3 Mining (OIII:TSXV)

MCAP – $107.2 million (at the time of writing)

Shares – 46,174,125

Cash – $32.0 million (approximately)

Strategic Shareholders – Osisko Mining 54.1%, Insiders 3.7%

The Genesis of O3 Mining

Earlier this year, Osisko Mining entered into a definitive agreement with Chantrell Ventures Corp (CV-H:TSXV), which saw Osisko’s non-core assets transferred to Chantrell, resulting in the Reverse Take-Over (RTO) of Chantrell by Osisko Mining.

The company was renamed O3 Mining, its shares were consolidated 40:1, it raised $18.6 million at $3.88 per share with a full warrant at $4.46, and the 3rd iteration of the Osisko team was born.

NOTE: For those who don’t know, the founders of Osisko Mining consists of John Burzynski, Robert Wares, Sean Roosen. Jose Vizquerra Benavides became part of the leadership team in 2011.

O3 Mining is led by CEO, Jose Vizquerra-Benavides, who is a geologist by trade. Vizquerra-Benavides is a native of Peru and comes from a long line of miners, as his grandfather is the founder of Buenaventura, a major mining producer company in Peru listed on the NYSE.

Vizquerra-Benavides began his career in the sector with Buenaventura, but eventually moved to Canada where he worked as a production and exploration geologist at the Red Lake gold mine.

From here, Vizquerra-Benavides joined the Osisko team where he has held a number of different roles or positions, such as Executive Vice President of Strategic Development & Director at Osisko Mining, and President & CEO of Oban Mining Corp.

While he is arguably the least known of the Osisko leadership team, I think that will soon change because, in my opinion, it’s obvious to me that Vizquerra-Benavides has the right pedigree to be successful in his new role as CEO of O3 Mining.

Quebec and Ontario

I’m not going to go into any detail about the jurisdictions, because unless you have been living under a rock or are new to resource sector investing, you will know that Quebec and Ontario are two of the best jurisdictions for mining investment attractiveness in the world.

The Fraser Institute continually has both jurisdictions rated in their top 20 places to explore, develop and mine worldwide.

Acquisitions

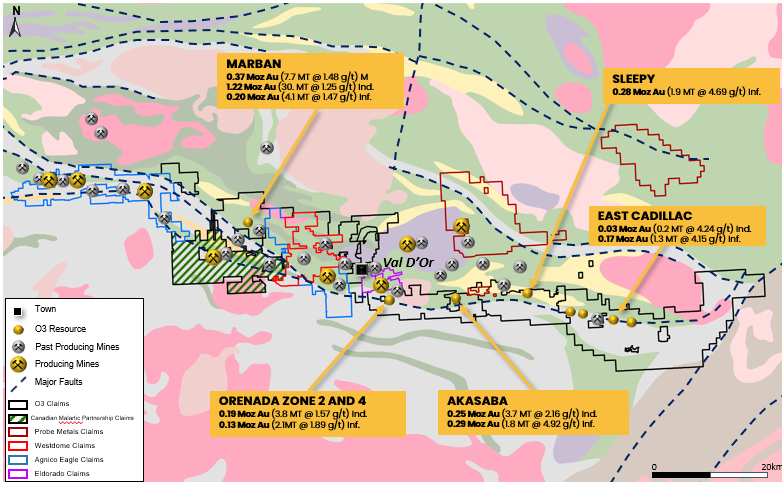

With the formation of the new company and Vizquerra-Benavides appointed as CEO, O3 didn’t waste any time adding to their already impressive land position within the Abitibi Greenstone Belt.

First was the acquisition of the Quebec subsidiary of Chalice Gold Mines Limited (details of the deal can be found here). A company with projects along the Cadillac Break.

NOTE: Chalice Gold Mines was acquired for $12.0 million in O3 stock.

Next, in another all shares deal, Alexandria Minerals was acquired (details of the deal can be found here). Clearly, given where O3 has focused their attention in their first drill program, Alexandria’s projects located in the Val d’Or region were particularly appealing.

NOTE: Alexandria Minerals had issued and outstanding 529,790,966 shares. O3 acquired Alexandria for $0.07 a share or 0.018041 for each O3 share, therefore, the purchase price was roughly $37.1 million.

Finally, in another all shares deal, O3 acquired Harricana River Mining Corporation, whose Harricana Mine Project is located in the Val d’Or area of the Cadillac Break (details of the deal can be found here).

NOTE: Harricana

was acquired for 773,196 shares in O3 with a stock price of $2.59 in the

announcement date – August 23, 2019. Therefore, the value of the transaction is

$2.0 million.

Figure 1: Val d’OR Consolidation – Post Acquisitions

Source: O3 Mining Inc.

Value of O3

In my opinion, protecting your downside risk is an integral part of consistently making profit from your investments within the junior resource sector.

Let’s do a quick calculation of O3’s underlying value:

- The total market value of O3’s acquisition is $51.1 million. Breakdown: Chalice Gold Mines – $12 million, Alexandria Minerals – $37.1 million, and Harricana River- $2 million.

- The RTO value of Osisko Mining’s non-core assets, which includes the advanced Marban project, was $99.9 million.

- O3 has raised a total of $37.78 million over the last 10 months: RTO financing – $10 million, Bought Deal financing (March 27th, 2019) – $17.7 million, Charitable Flow-Through financing (September 26th, 2019) – $10.08 million

Therefore, if you add up the value of O3’s acquisitions, Osisko’s non-core project portfolio and their cash (which will be lower than the total amount that they raised), the underlying value of O3 Mining is roughly $200 million or almost twice the current MCAP.

NOTE: No value is assigned to the exploration potential.

In my opinion, while the share price can undoubtedly move lower, I like the downside protection which O3 presents at its current price.

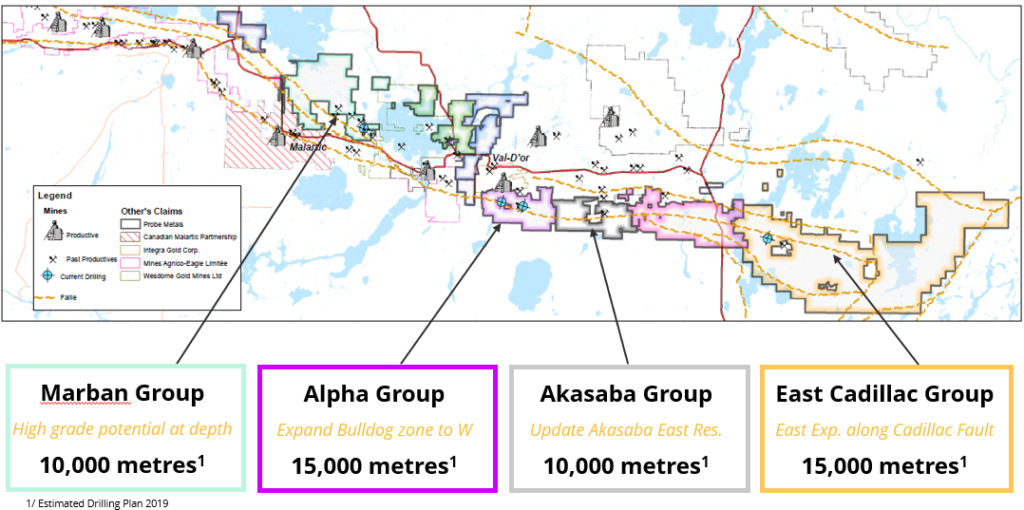

Drill Targets

With the acquisitions in place, O3 is continuing to march forward with a 50,000m drill program on 4 main target areas within their Val d’Or region properties.

Figure 2: Aggressive Osisko Style Exploration

Source: O3 Mining Inc.

The drill program is being funded by a $10.08 million charitable flow-through private placement which closed on September 26th.

For those who don’t know about charitable flow-through shares, they’re typically issued at an even higher multiple above the market share price value than regular flow-through shares.

The ability to raise cash through charitable flow is a tremendous advantage compared to a regular hard dollar private placement, as it reduces the amount of dilution by the raise, while also giving the buyer an even higher tax reduction for participating.

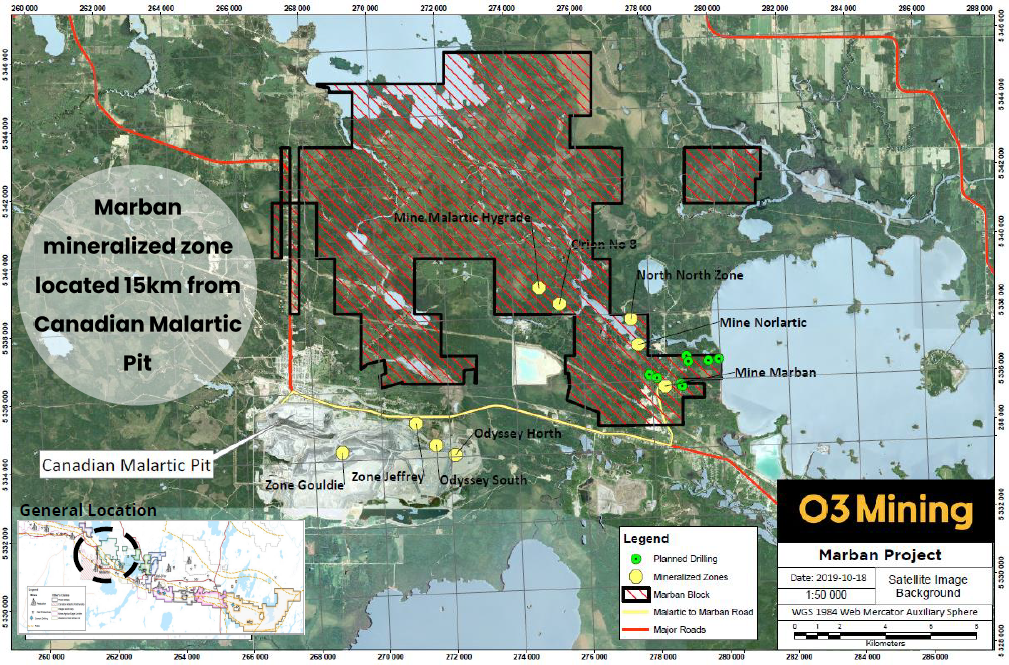

Marban Group

The Marban Group consists of the Marban and Harricana projects. The Marban project is located near the town of Malartic, Quebec, which sits roughly 30 km west of Val d’Or.

It’s one of the non-core assets which was spun out from Osisko Mining in the RTO with Chantrell Ventures. Marban was originally acquired by Osisko (Oban Mining at the time) from Niogold in 2016 when the 2 companies merged.

Marban has a 43-101 in-pit measured and indicated resource of 37 Mt at 1.24 g/t for 1.48 Moz of gold and an in-pit inferred resource of 3.6 Mt at 1.15 g/t for 0.13 Moz of gold.

In my conversation with Vizquerra-Benavides, O3 is planning to drill 8 holes there, which will be targeting high-grade gold below the existing resource – which means below 400m.

For those who aren’t familiar with Abitibi shear zone gold deposits, they can be deep, high grade and steeply dipping.

Therefore, exploration below 400m for high-grade gold mineralization is a legit prospect and one that I am very interested to see tested.

Figure 3: Marban Project

Source: O3 Mining Inc.

Additionally, as mentioned earlier, Marban is located in close proximity to the town of Malartic, which also means it’s in close proximity to the Canadian Malartic Open Pit Gold Mine owned by Agnico Eagle and Yamana Gold.

It is speculation, but I believe it’s valid to think that Marban becomes an attractive acquisition target for the Canadian Malartic Mine moving forward, as its reserves dwindle and precious metal prices remain strong.

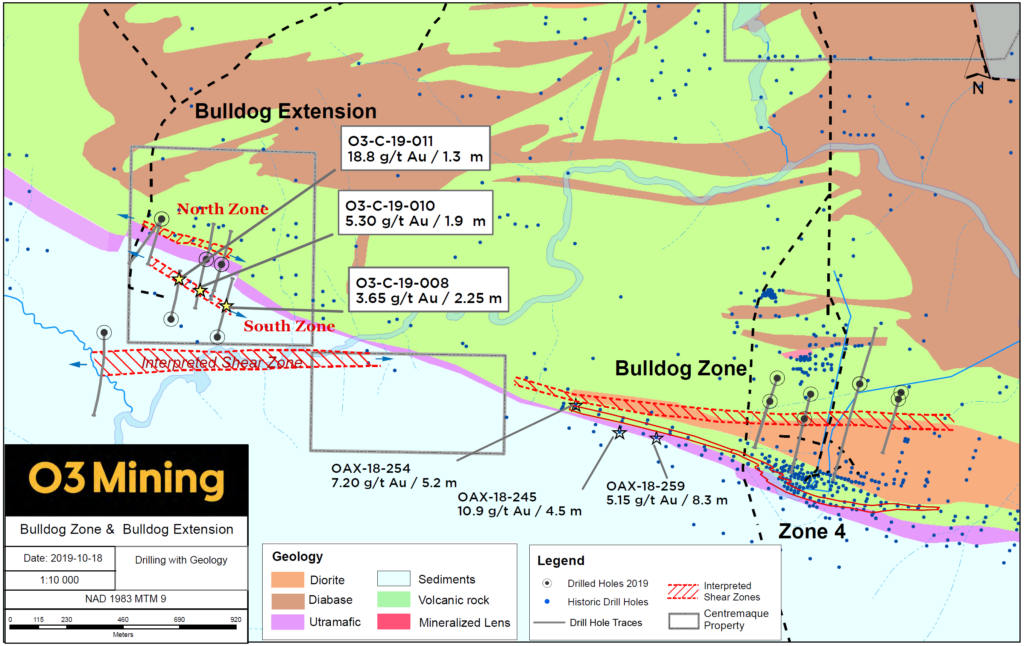

Alpha Group

The Bulldog zone was discovered by Alexandria Minerals in late 2018.

Reviewing the results in the December 11th, 2018 news release, the Bulldog zone is east-west trending and has been confirmed over 500m with a thickness ranging from 20 to 40 metres.

There were 8 initial holes drilled on the Bulldog target in 2018 and they returned some great results, which were highlighted by:

- Drill hole OAX-18-245 intersected 10.50 m @ 6.20 grams per tonne (g/t) Gold (Au) including 4.50 m @ 10.87 g/t Au.

- Drill hole OAX-18-254 intersected 10.50 m @ 4.25 g/t Au including 5.20 m @ 7.20 g/t Au.

- Drill hole OAX-18-259 intersected 8.30 m @ 5.15 g/t Au and 3.00 m @ 6.92 g/t Au.

With regards to drilling at Bulldog, Vizquerra-Benavides mentioned the phrase, “drill for structure, drift for gold”. Meaning, first and foremost, they want to establish or understand the structures that are controlling the gold mineralization.

Early this week, O3 announced results that confirm the extension of the Bulldog mineralized structure located 1,500 metres to the east and importantly, demonstrate the potential for gold-bearing structures in the Pontiac sediments.

The Bulldog gold-bearing mineralized structure discovered in December 2018, demonstrates good continuity in gold grades over several metres and is over 500 metres in strike length.

- Drill hole O3-C-19-011 intersected 18.8 g/t Au over 1.3 metres

- Drill hole O3-C-19-010 intersected 5.30 g/t Au over 1.9 metres

- Drill hole O3-C-19-008 intersected 3.65 g/t Au over 2.25 metres

Figure 4: Alpha Group – Bulldog Zone

Source: O3 Mining Inc.

O3 will continue with its 15,000m drill program in the Alpha Group, systematically drilling every 80 meters across the known zone, with the intent of establishing an inferred resource.

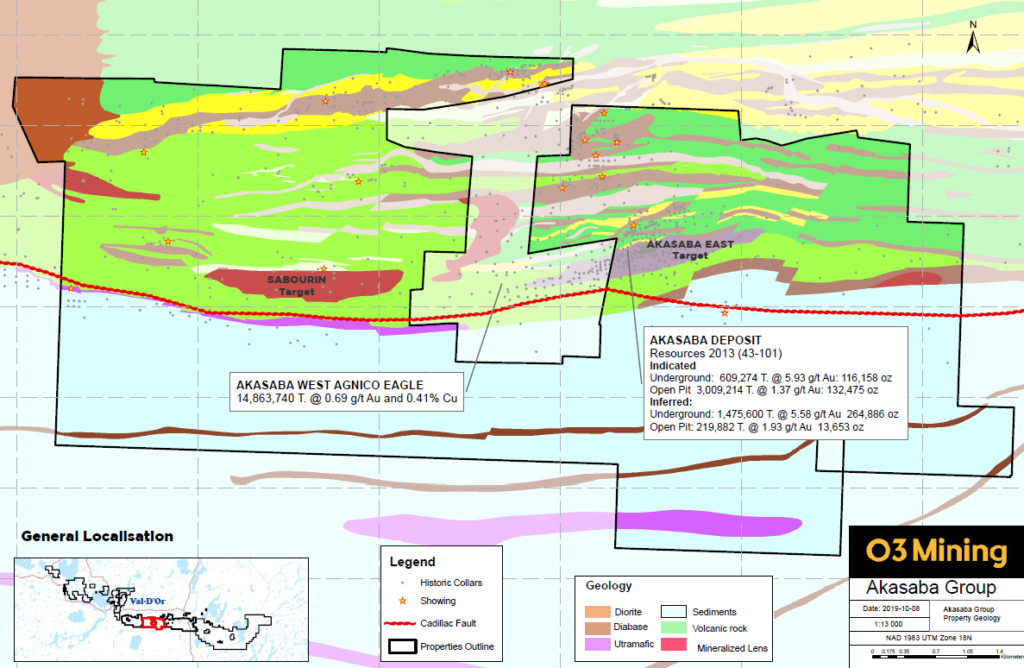

Akasaba Group

Akasaba sits east of the Bulldog Zone and, of course, on the east side of Akasaba West, which is an open-pit development project owned by Agnico Eagle. Akasaba West has an inferred resource of 14.8 Mt at 0.69 g/t for 332,074 oz of gold and 0.41% for 61.2 Mkg of copper.

O3 will perform a 10,000m drill program in the Akasaba Group

to confirm and expand resources in the Akasaba east target.

Figure 5: Akasaba Group

Source: O3 Mining Inc.

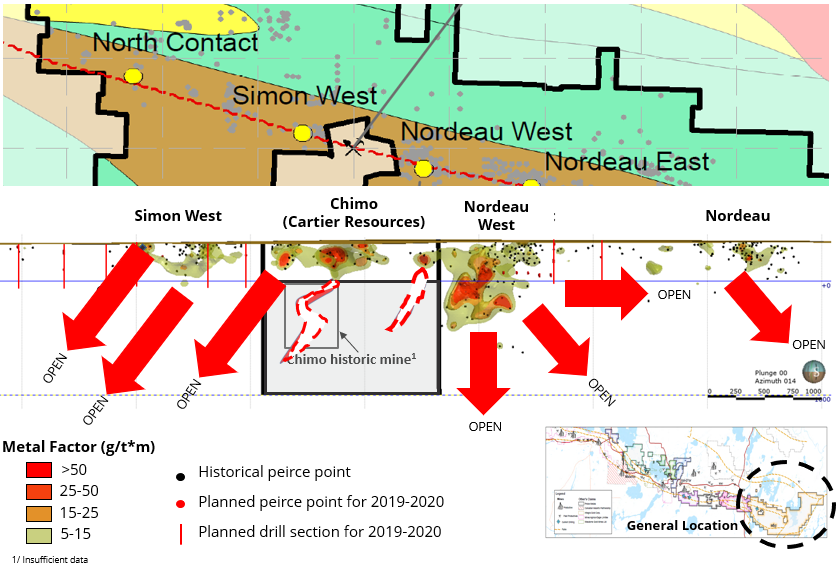

East Cadillac Group

The Nordeau West target in the O3’s East Cadillac Group, which was acquired in the acquisition of Quebec portion of Chalice Gold Mines, sits to the east of Val d’Or and of O3’s other 3 drill target areas.

Nordeau West has a JORC

indicated resource estimate of 225,000 tonnes at 4.17 g/t for 30,200oz of

gold and an inferred resource of 1.112 Mt at 4.09 g/t for 146,300 oz of gold.

Figure 6: East Cadillac Group

Source: O3 Mining Inc.

As you can see in the image above, O3 now controls essentially all of the land which surrounds the historic Chimo Mine, which is owned by another junior gold company – Cartier Resources (ECR:TSXV).

If you take the time to review the 3D resource model which is available on VRIFY’s website or in the video on Cartier’s website, you will get a good idea of the deposit and how it relates to the prospects on O3’s property.

Given the existing resource on the Nordeau West target and where O3 will be targeting their drilling, there’s a good chance that gold mineralization, possibly high grade, will be discovered.

Concluding Remarks

As I mentioned in the intro, success in the junior resource sector, I believe, is predicated on 3 main factors.

First, invest in the best people.

- O3 Mining is the 3rd iteration of the Osisko Mining Group and is led directly by its CEO, Jose Vizquerra-Benavides. The Osisko team has made it a habit of being successful in an industry that is fraught with failure.

- Not only have they done it at the peak of the market – bringing the Canadian Malartic Gold Mine into production in 2011, but they have also raised over $400 million dollars to develop the soon-to-be-feasibility-study-level Windfall project over the course of one of the worst bear markets in history.

Second, protect your downside risk.

- O3 is currently selling for roughly half of its intrinsic value, providing the investor with good downside risk.

And, finally, take a contrarian view of the market and/or the company.

- Most of the junior resource sector is selling off, including O3 Mining, which has seen its share price reach a low below $2.30 a share, over the last month or two.

- “Be fearful when others are greedy and greedy when others are fearful” ~ Warren Buffet

There is risk in any investment, especially when it comes to mineral exploration, but by sticking to the highest quality issuers, I believe, you give yourself the best opportunity for profit!

I own shares in O3 Mining and will continue to buy on weakness in the weeks ahead.

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I have NO business relationship with any of the companies discussed in this article. I do own shares O3 Mining and Cartier Resources.

A Look at Nickel & Why It’s The Best Performing Metal of 2019

The majority of resource sector investors are currently focused on precious metals, which I think is justified. Whether it be a trade war, the issuing of 30 year bonds with a negative yield, or the lowering of interests rates, clearly, there are issues with the global financial system that need to be rectified.

Precious metals, therefore, are acting like any insurance policy; their price is rising along with the increase in risk.

With that said, nickel has actually been the best performing metal of 2019 to date. Its price has risen more than 50% in the last 2 months and, today, sits at around US$8 per pound – a level not seen since 2014.

I have become well acquainted with the nickel market over the last few years and am really not surprised by the sudden price move; to me, it was inevitable. There are a number of factors that could drive the nickel price even higher in the future, the export ban in Indonesia being just one of them.

Today, I have for you an interview with someone who lives the nickel market every day, Martin Turenne, CEO of FPX Nickel Corp.

In our conversation, we touch on the history and strategy behind the Indonesian export ban, the various nickel end products in the market, global nickel inventories, the affect of the environmental policy moving forward and, finally, an update on FPX Nickel, which has recently released some fantastic news with regards to the Baptiste Deposit’s metallurgy.

Enjoy!

Brian: Many of the headlines surrounding this recent surge in the nickel price have concentrated on the Indonesian export ban and for good reason. In 2014, Indonesia introduced the first export ban and within 6 months the nickel price spiked above US$9 per pound. Now, 5 years later and the same scenario appears to be playing out.

Firstly, could you give us some historical background on why Indonesia instituted a nickel export ban in 2014?

Martin: Indonesian mines produce about 25% of the world’s nickel mine supply, but the country has traditionally been lacking in domestic refining capacity – for a long time, they were simply shipping low-value, unprocessed ore to refineries in China. Indonesians have a long history of resource nationalism, and the export ban in 2014 was implemented to force companies to build smelters in Indonesia so that the country could enjoy more of the economic benefits of producing refined nickel — to generate economic activity from capital investment and job creation. The ban was at least partly successful in achieving that goal – Indonesia is now a major producer of refined nickel.

Brian: Secondly, why are they having to ban exports again? Did the 2014 ban not produce the results they had intended?

Martin: After implementing the ore export ban in 2014, the Indonesian government partially relaxed the ban in 2017 to allow for the export of some ore by those companies which had committed to building smelters in-country. The buildout of those smelters was moderately successful, but it wasn’t happening as quickly as the Indonesian government would like it to. So, the re-implementation of a full ban is driven in part by the Indonesian government’s desire to force companies to act more swiftly in building out those smelters.

Brian: Background context is important, but really, what matters to investors is the impact of the export ban.

What is the impact of the export ban on the global market supply?

Martin:

There has been some good analysis come out in the past few days from BMO and Wood Mackenzie which concludes that the export ban will result in a 5-10% reduction in nickel supply for the next 2-4 years, versus their previous supply assumptions. The nickel market has already been in a long-term structural shortage since 2016, so this additional supply disruption is a major event. This could lead to the nickel price being sustainably higher for the next few years.

Brian: Examining the nickel price chart, while initially, instituting the nickel export ban in 2014 spiked the price, the impact seems to have dramatically declined in the second half of the year, bringing the price back to where it started at the end of 2014.

Today’s market looks much different than it did in 2014 – for a number of reasons. The first thing that comes to my mind is global nickel inventories, which are nearly half the levels in 2014.

For example, looking at the LME nickel warehouse levels, it shows that current inventory is sitting at roughly 150,000 tonnes.

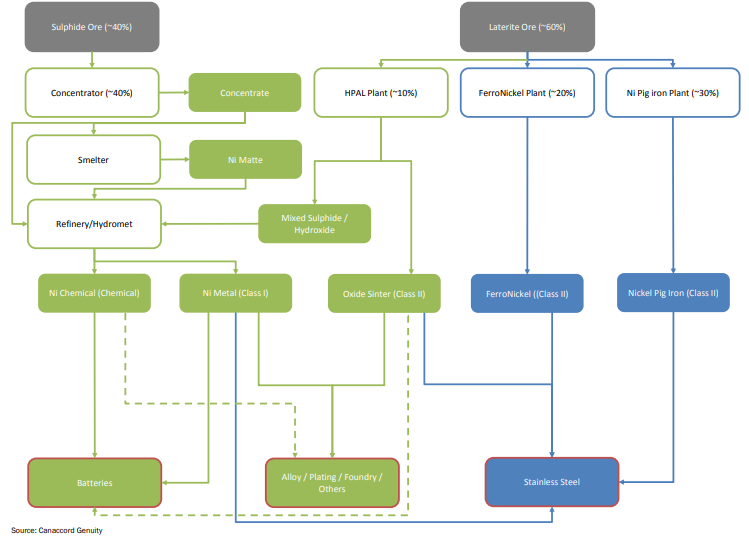

An important question rarely asked, possibly out of ignorance, is what type of nickel makes up the Global inventories?

Martin: LME inventory is comprised entirely of Class 1 nickel products, typically briquettes, pellets and cathode – to qualify as a Class 1, the nickel product must contain 99.8% nickel, so basically pure nickel.

Brian: Okay, this brings us to a common misconception, that nickel sulphide mines produce class 1 nickel, which is incorrect.

So it begs the question, who does feed the Class 1 nickel market?

Martin:

As I’ve said, Class 1 nickel is basically a pure nickel product. Class 2 nickel products have less nickel content, but they contain significant amounts of iron, which makes them highly sought after by stainless steel producers.

Class 1 nickel comes from both sulphide and laterite nickel mines. For both sulphide and laterite ore, there are several refining and processing steps required to convert the ore into a concentrate or slurry and then ultimately into Class 1 nickel – oftentimes, it’s the refiners and smelters who enjoy better margins than the actual miners themselves. That’s part of the reason that the nickel industry tends to be vertically integrated – if you’re a miner having to sell your product to a third party smelter, you are at the mercy of smelter payment terms.

Brian: Can you give us a break down of the most common end products produced by mining operations and how they fit into the global nickel market supply?

Martin: The nickel produced at most mine sites is not Class 1 nickel – sulphide miners typically produce nickel concentrate with about 15% nickel content, and laterite miners mostly produce Class 2 nickel in the form of ferronickel or nickel pig iron (NPI) with a nickel content ranging between 10% and 30%. Nickel sulphide concentrates are typically sold for a relatively low value (70-75% of the LME nickel price) to smelters, who then smelt and refine the nickel toward the ultimate production of a Class 1 nickel product. Ferronickel and NPI, on the other hand, bypass the smelting process and are sold directly to stainless steel producers for relatively high value (95-100% of the LME nickel price) due to the value of the iron contained in those products.

Brian: Keeping with the nickel supply side discussion, recently it was reported that there was a waste spill from the Chinese owned Ramu nickel mine in Papua New Guinea. The red discharge spilled from the mine was found clouding the waters of Basamuk Bay.

Personally, I only see the environment becoming a bigger issue in the future, as it’s become a hot politically driven subject.

Do you think more stringent environmental regulations will affect nickel supply in the future? If so, please explain.

Martin: In the last year alone, we’ve seen environmental and social issues lead to the closure or the threatened closure of mines in Papua New Guinea, Myanmar, Guatemala and Brazil – and that’s to say nothing of the ongoing environmental inspections in the Philippines, which is one of the largest producers of nickel globally. Well over 60% of nickel mine supply comes from emerging economies with lower environmental and social licence standards than say, Canada or Australia. As environmental and social concerns become more prominent in those emerging countries, that will ultimately lead to either the closure of certain nickel mines, or to increased operating costs for miners having to comply with higher standards. Over time, this will lead to an increase in the nickel cost curve, and therefore in the nickel price.

Brian: We have discussed all supply side issues within this interview on the current nickel market, which, in terms of gauging how strong the nickel market could be, it’s supply driven bull markets that are the strongest.

None of us have crystal balls, but in your opinion, is it realistic to think that we will see nickel prices higher than US$7.50 over the next 12 months?

Martin: Before the recent announcement regarding the Indonesian export ban, the long-term consensus nickel price forecast was $7.50/lb. The implementation of the export ban has accelerated the spot price move upward. We would expect to see more volatility in the nickel price over the next 12 months, but the updated forecasts from BMO and Goldman Sachs are already projecting an $8 to $9 price in that timeframe.

Brian: A few weeks ago, FPX released the results of their metallurgical optimization program which began late last fall. In my opinion, the results look great and should give the company a relatively unique end product which can bypass the smelter and be sold directly to the end user.

Firstly, can you give us an overview of the results? Secondly, can you speak to the possible benefits of being able to bypass the smelter?

Martin: The new metallurgical results mark a huge breakthrough for FPX. First, we are seeing recoveries in the range of 83-94%, which is a big improvement over the 82% recovery in the 2013 PEA – this will lead to an increase in projected nickel production and lower the unit cost of production. Second, we are now producing a separate iron ore by-product for the first time in the project’s history; depending on the market for our iron concentrate, this new product stream could have a positive impact on project economics. Third, the nickel concentrate we are now producing grades 63-65% versus the 13.5% concentrate in the previous PEA. Producing this high-grade concentrate means we will likely get paid a lot more for the product, something in the range of 90-95% of the LME nickel price, compared to the 75% payability assumption in the previous PEA. That’s because this high-grade concentrate is very low in penalty elements like sulphur and phosphorus, which means it will by-pass smelters and can be directly fed to stainless steel producers. By cutting out the smelter middle man, we can yield the types of payables achieved by similar products like ferronickel and NPI.

Brian: The metallurgical results certainly didn’t go unnoticed, as FPX’s recent private placement was oversubscribed. Now, with the influx of cash and the work completed over the last few years, I assume we may be headed for an update to the 2013 PEA in 2020.

What is the plan for 2020? Will we see an update to the 2013 PEA? Do the plans for 2020 require there to be sustained high nickel prices?

Martin:On closing our current private placement, we will have over $2 million in the treasury and will be fully funded to execute on more metallurgical test work, particularly leach testing of the nickel concentrates to understand if we can produce nickel in a form suitable for the EV battery market. Beyond that, and assuming the nickel price settles above the $7.00/lb level, we will be well positioned to deliver an updated PEA, with exact timing still to be confirmed.

Concluding Remarks

There is much to be gleaned from Turenne’s answers in the interview. In my opinion, many of the topics that we discussed are often over looked or misunderstood by investors. With this new or clarified knowledge of the nickel market dynamics, I think nickel investors are in a much better position to make informed investment decisions.

With that said, in my opinion, you should never buy a junior resource company because you are bullish on the price of the metal. Remember, junior resource companies are businesses that revolve around the people and their ability to execute on a plan which reflects the company’s overall vision.

If management can’t execute, nickel deposits don’t get discovered or developed and, therefore, no matter where the nickel price goes, you are most likely going to lose money.

I’m bullish on the future of nickel and, at the moment, am only invested in one junior nickel company – FPX Nickel Corp. (FPX:TSXV).

For those interested in knowing more about the nickel sector and why I believe FPX presents great risk to reward potential, check out these links:

2019 VRIC Presentation – Nickel: A Short and Long-Term Outlook

Nickel Laterite’s Integral Role in the Coming Nickel Boom

KE Report – Taking Note of the Run in Nickel

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I have NO business relationship with FPX Nickel Corp., however, I do own shares.

Quebec Site Tour Visit Day 2 – Cartier Resources

Day 2 began at Cartier Resources’ offices in Val d’Or. Interestingly, Cartier’s office walls are filled with field work photos, Chimo mine blueprints, deposit layouts, historical Val d’Or mining statistics and a whole host of other interesting pictures.

Personally, I thought this was a nice touch for visitors as it gives a good perspective on what the company has and is doing to move the company forward – a picture is worth a thousand words.

Cartier Resources (ECR:TSXV)

MCAP – $30.1 million (at the time of writing)

Shares – 177.1 million

Cash – roughly $6 million

CEO – Phillippe Cloutier is a geologist by trade with over 25 years of experience in mining exploration and development.

Cartier’s Business Plan

Cartier made it clear that using funds efficiently is their top priority; they started their presentation by outlining how they go about their exploration work with an added focus on how they planned their drill programs on the past producing Chimo mine property.

The talk was led by VP Dr. Gaetan Lavalliere, who is a professional geologist with over 25 years of experience in the mining industry.

Cartier organizes their geological data to formulate a prioritized list of targets. By doing this, they are always focused on the targets that have the highest probability of returning good results for each dollar spent.

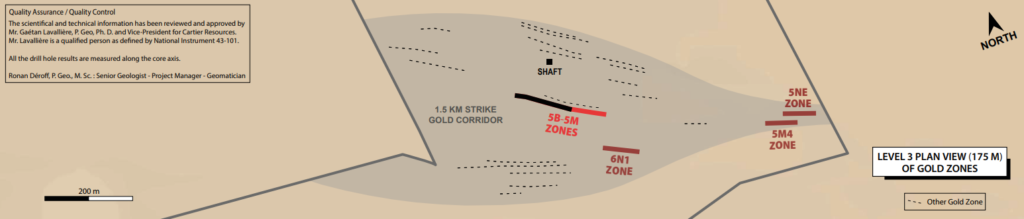

With regards to Chimo, the team was focused on 3 high priority targets from the deposit’s 24 zones.

It should come as no surprise that these zone extensions are mostly at depth, which fits the Abitibi shear zone related gold deposit model. Each of the companies that we visited on our trip were focused on targeting high grade gold mineralization at depth.

I believe Osisko’s ‘Discovery 1’ hole could prove to be a major catalyst for all the other companies with gold projects along the Abitibi, to follow suit and explore deeper…much deeper.

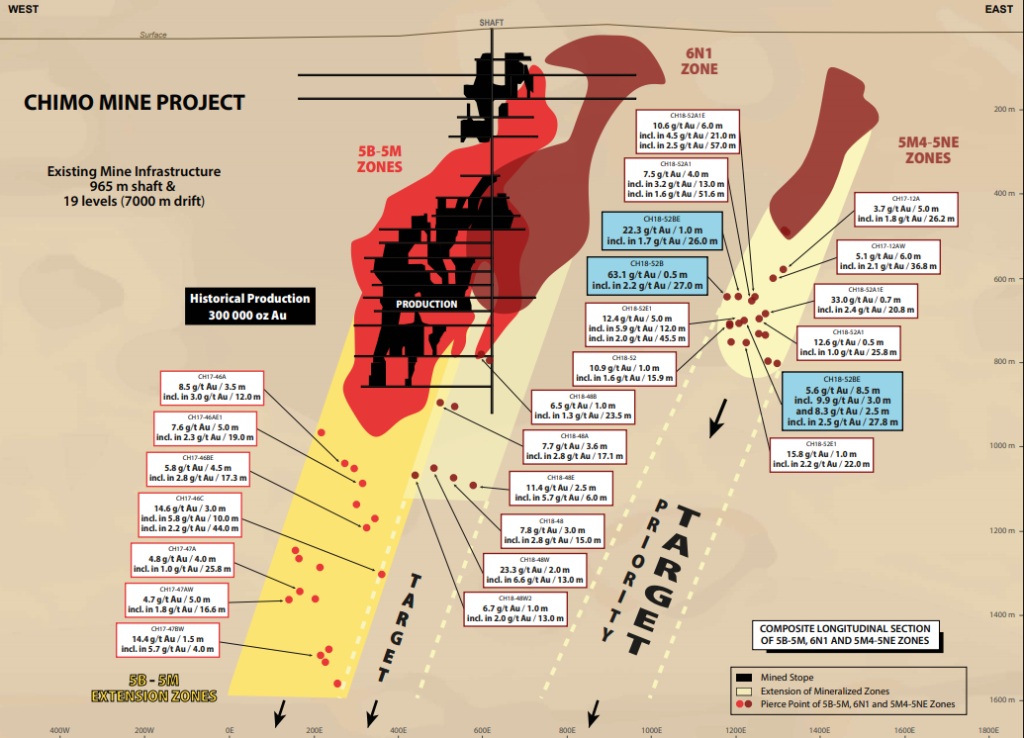

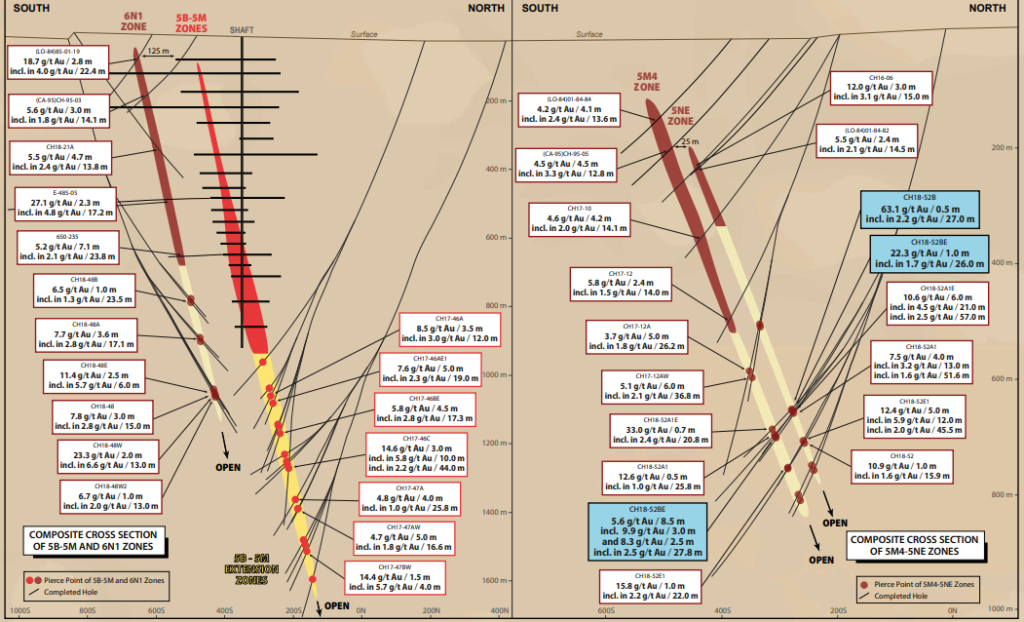

Cartier’s zone extension drilling, in my opinion, has been a success with some very good grades and widths. Reviewing the images above, which were provided by Cartier, you can clearly see how the drilling was systematically planned to delineate the gold mineralization.

If I were to have a criticism of Cartier, it would be that they don’t have any 43-101 technical reports supporting what they have done at Chimo. To explain that further, I fully subscribe to the fact that any senior company interested in Chimo will disregard any technical report Cartier possessed in favour of conducting their own due diligence.

Moreover, most sophisticated investors in the sector can review the drill results and historical mine data and construct an economic model for the revitalized mine and have an idea of its potential value.

The problem, at the moment, is the company says they are targeting the retail market, who, by and large, don’t have the necessary skills to calculate the value of Chimo. Instead, they are depending on someone else’s opinion to gauge its potential value.

NOTE: On a high level, to model Chimo effectively, you would need to have a grip on two important points; the resource size and grade and cost of dewatering the flooded shaft and underground workings. With realistic values for these 2 points, you could model the project using the costs and tax structures from other economic studies or mines in the general Val d’Or area.

In open discussion with CEO Cloutier, this point hasn’t been overlooked by the management team. They are now, however, in a position that requires them to conserve money and await a buyer for Chimo. The conservation of cash allows Cartier to weather any storm that may be headed their way when it comes to negotiation for Chimo.

Takeover Candidates

Who would be a likely candidate to purchase Chimo?

That’s a great question and one that’s key to Cartier’s investment proposition.

First and foremost, the obvious candidate is O3 Mining, which, over the last month or so, has bought up a ton of land around Chimo, through their purchases of Chalice Gold Mines and Alexandria Minerals.

O3 Mining is a new company formed by the Osisko Mining team, whose track record supports an aggressive approach to all aspects of mining company development.

In my opinion, if O3 were interested in Chimo, it wouldn’t be for the short-term production capability, it would be because they see the potential for a much larger system in the area, Chimo just being one of the key pieces.

Additionally, I have heard Agnico Eagle’s name come up as a potential suitor for the purchase of Chimo. I’m less inclined to believe they are a better candidate than O3 to make the purchase, because Chimo, at this point, is much smaller in both resource size and land position than would typically entice a major’s attention.

While O3 and Agnico are arguably the top takeover candidates, it could be a much smaller producer with underground experience that is willing to take on this small short-term production capability story, but they will have to be well financed to make it happen.

Time will tell.

Concluding Remarks

Personally, I do see the value in owning Cartier, even without having modelled Chimo. They are cashed up, have a good management team, and have a bunch of other high potential projects that are just waiting in the wings as far as exploration goes.

Without a doubt, there will be a buyer for Chimo, it’s just a matter of price and when it will happen.

A potential investor must realize that a deal may not be imminent and understand that Cartier will be in hibernation mode until a deal can be made. Depending on your investment outlook and level of patience, this could be a deal breaker.

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I have NO business relationship with Cartier Resources, nor do I currently own any shares. However, all of my expenses for the site visit were paid for.